Learn 7 ways to verify reputable roofers near me—insurance checks, real reviews, photo documentation, and itemized estimates—before you hire.

Typing reputable roofers near me into Google after a hailstorm or a slow leak feels like a gamble. Every company website says the same thing: family-owned, honest, quality work. You can't tell who actually backs that up until a crew is already on your roof, and by then it's too late to change your mind.

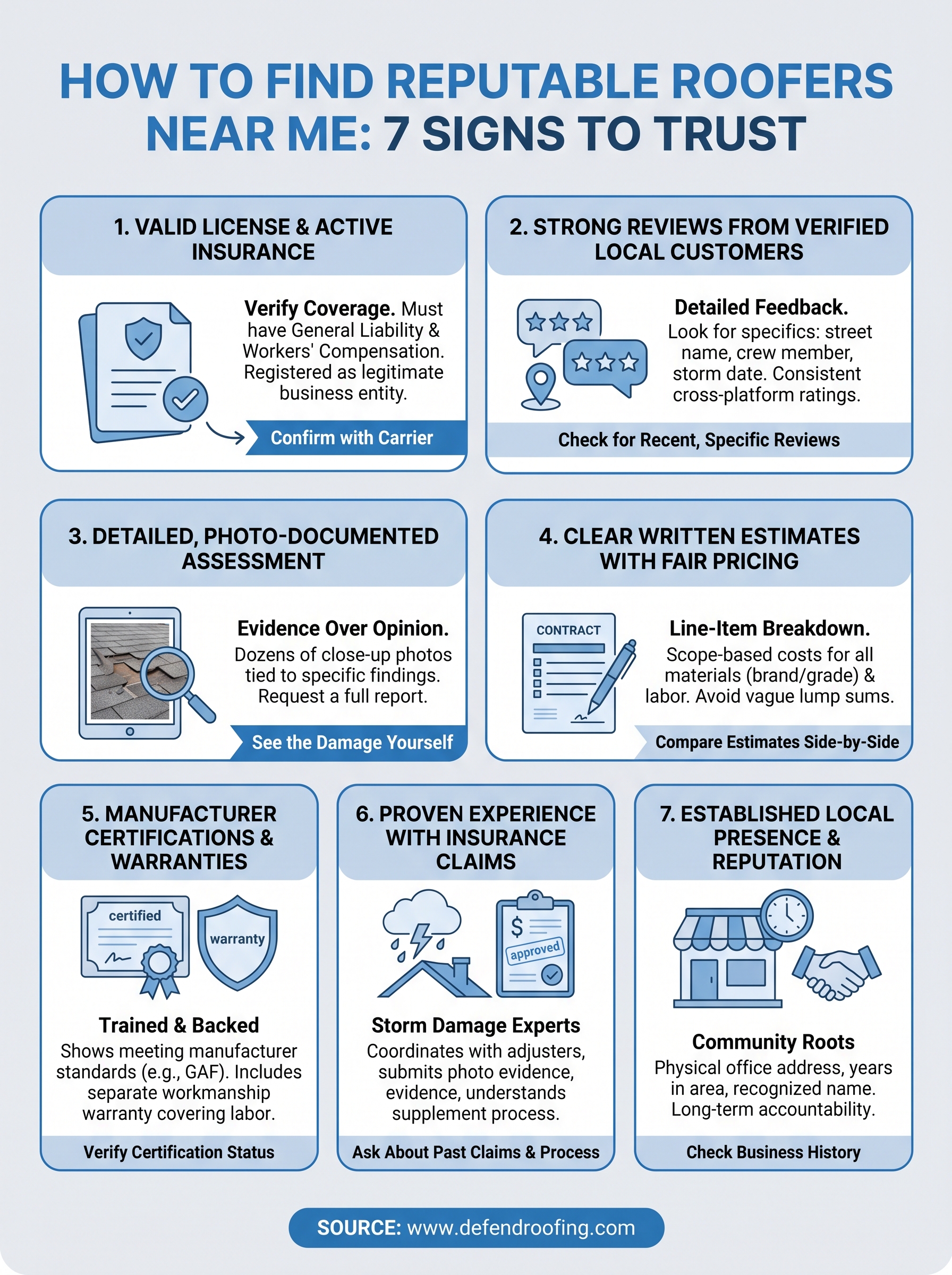

The real answer isn't another list of five-star reviews. It's a set of concrete signs you can check before you sign anything: licensing and insurance you can verify, documentation that shows the actual condition of your roof instead of a verbal opinion, manufacturer certifications, and a written scope that matches what gets billed. Contractors who skip these steps usually skip the hard parts of the job too.

We've spent three generations doing roof work in Central Texas, so we've seen what separates a trustworthy contractor from a truck-and-ladder outfit chasing storm damage. Below are seven signs that hold up under scrutiny, so you can compare local roofers with actual confidence instead of hoping the reviews are real.

Texas doesn't require a statewide roofing license, which surprises a lot of homeowners. That gap is exactly why insurance verification matters more here than in states with strict licensing boards. Anyone with a truck and a ladder can call themselves a roofer in Central Texas, so the burden shifts to you to confirm the company carries real coverage before they touch your shingles.

A reputable contractor carries general liability insurance and workers' compensation coverage, and they'll hand you a certificate of insurance (COI) without hesitation. They're also registered as a legitimate business entity with the Texas Secretary of State, not operating under a random name they picked up last season. Ask for proof and watch how fast it shows up. A company with nothing to hide sends it within minutes, often before you even ask twice.

If a roofer stalls when you ask for proof of insurance, that hesitation is the answer.

Without workers' comp, you're financially exposed if a worker gets hurt on your property. Without general liability, you're the one paying if a crew damages your siding, cracks a window, or leaves a mess that costs thousands to fix. Underinsured contractors often price jobs lower because they're not carrying the overhead of proper coverage, and that gap gets passed to you the moment something goes wrong. This isn't a hypothetical. Roofing consistently ranks among the more dangerous trades tracked by the Occupational Safety and Health Administration, which is exactly why coverage isn't optional for a company doing this work seriously.

Don't take a verbal assurance. Ask for documentation and confirm it independently before signing anything.

| Coverage type | What it protects | Who's exposed without it |

|---|---|---|

| General liability | Property damage during the job | Homeowner |

| Workers' compensation | Injuries to crew on your roof | Homeowner and crew |

| Business registration | Legitimate, traceable ownership | Homeowner seeking recourse |

A five-minute phone call to a carrier costs you nothing and tells you more than any sales pitch. Skip this step and you're trusting a stranger's word on a project that involves ladders, nail guns, and your home's biggest physical asset.

Reviews are easy to fake and easy to buy, so the number of stars matters less than where those stars come from. A reputable roofer near you should have a track record of reviews tied to actual jobs in your area, not a generic five-star average padded with vague comments from accounts with no history.

Look for reviews that mention specifics: a street name, a storm date, a crew member, or a particular repair. Verified local reviews read like they came from a real homeowner describing a real job, not a template. Volume matters too. A contractor with 150 reviews earned over several years across Cedar Park, Avery Ranch, and Leander tells you more than one with 12 reviews posted in the same week.

A handful of specific, detailed reviews beats a wall of generic five-star ratings every time.

Review patterns expose how a company actually treats customers once the contract is signed, not just how they pitch the job. A cluster of reviews complaining about pushy upselling or disappearing crews is a warning sign no sales rep will mention. Consistent feedback across platforms and years shows a company that's been accountable to the same community long enough to build a reputation worth protecting.

Don't stop at the star rating on one platform. Cross-check the pattern before you trust it.

A verbal opinion about your roof's condition isn't evidence, it's just an opinion. Photo documentation turns a guess into proof, and it's one of the clearest ways to separate contractors who want to earn your trust from ones who want your signature fast. If a company walks your roof for ten minutes and hands you a one-page quote with no pictures, you have no way to check their work against reality.

A thorough inspection produces dozens, sometimes over a hundred, close-up photos covering every slope, valley, vent, and flashing point on your roof. Precision documentation means each photo is tied to a specific finding, like a cracked pipe boot or granule loss on the south-facing slope, not a random collection of shots taken for show. You should walk away with a report you can actually read, not a verbal summary you have to take on faith.

If you can't see the damage in a photo, you shouldn't be paying to fix it.

Documentation protects you twice. First, it lets you confirm the recommended work matches actual damage instead of a sales quota. Second, if you're filing an insurance claim, adjuster-ready photos speed up approval and reduce disputes over what's covered. Honest assessments built on evidence also catch the difference between a roof that needs a targeted repair and one that genuinely needs full replacement, which matters when a contractor has no incentive to inflate the scope.

Ask to see the photos before you agree to anything, and expect a report you can keep for your own records.

A verbal number scribbled on a business card isn't an estimate, it's a guess you can't hold anyone to later. Written estimates protect you from the classic bait-and-switch, where a low initial quote balloons once the crew is already tearing off shingles and you're stuck negotiating from a weak position.

A fair estimate breaks the job into line items: tear-off, decking repair if needed, underlayment, shingles or metal, flashing, ventilation, and cleanup. Scope-based pricing means every cost ties back to a specific task tied to your roof's actual condition, not a flat number pulled from a formula based on square footage alone. You should see materials specified by brand and grade, not vague terms like "standard shingles."

A price you can't break into line items is a price you can't trust.

Vague pricing gives a contractor room to add "surprise" charges once the job starts, and homeowners rarely have leverage to push back once a roof is half torn off. Fair pricing reflects the actual scope uncovered during the assessment, not an inflated number designed to leave room for upselling or a lowball designed to win the bid and pad the invoice later. A contractor who prices honestly from the start has already shown you how they'll treat every decision that follows.

Compare estimates side by side and question anything that reads like a placeholder.

A contractor confident in their pricing will walk you through every line without getting defensive. That's the difference between a fair quote and a number designed to close the deal fast.

A roof is only as good as the materials and the install behind it, and warranties are where that gets tested. Manufacturer certifications show a contractor has met training standards set by companies like GAF or Owens Corning, while a workmanship warranty covers the labor itself, which the manufacturer's paper never touches. Skip either one and you're gambling on a roof with no real backup if something fails five years from now.

Certified contractors display their status prominently, usually GAF Master Elite or a comparable tier from Owens Corning, CertainTeed, or Malarkey. Extended manufacturer warranties on materials and labor are only available to contractors who've passed installation training and maintain a clean claims history. Alongside that, look for a limited lifetime workmanship warranty from the company itself, covering their own labor separately from the shingles or metal panels.

A manufacturer warranty without a workmanship warranty only covers half the problem.

Most roof failures trace back to installation error, not defective shingles, which is why the labor warranty matters as much as the material one. Without it, you're stuck paying for repairs on a roof that's technically still "under warranty" from the manufacturer's side. Certified installers also tend to follow manufacturer specs on ventilation and fastening patterns, details that determine whether a roof lasts 20 years or fails at year eight.

Don't accept a warranty claim without checking it against the manufacturer's own records.

Hail and windstorms roll through Central Texas every year, and after one hits, your neighborhood fills up with unfamiliar trucks and magnetic door signs. Storm chaser roofers show up for a few weeks, sign as many contracts as possible, and disappear before the first callback on shoddy work. A reputable roofer has weathered claims season after season in the same zip codes, which means they know how the adjuster process actually works, not just how to knock on doors.

A contractor with real claims experience talks about the process specifically: how adjusters scope damage, what documentation they expect, and how supplement requests get filed when the initial estimate misses something. Insurance-savvy contractors meet the adjuster on-site when possible and hand over photo evidence that matches the carrier's own damage criteria. They also tell you plainly when damage doesn't meet the threshold for a claim instead of encouraging you to file one anyway.

A roofer who's only worked one storm season isn't the one you want handling your claim.

Insurance claims live and die on documentation and timing. A contractor unfamiliar with the process can miss a supplement deadline or fail to capture damage the way an adjuster expects, and that gap comes straight out of your payout. Adjuster coordination done well means fewer disputes, faster approval, and a claim that actually covers the real scope of repair instead of a lowball settlement you're stuck negotiating alone.

Ask pointed questions about past claims before you sign anything.

A roofer with a real address and years of history in your neighborhood has something to protect that a fly-by-night crew doesn't. Local presence means the company has a physical office, a phone number that gets answered by a person, and a name your neighbors already recognize from yard signs or word of mouth. That kind of visibility isn't proof of quality on its own, but it's a lot harder to fake than a slick website built last month.

Established contractors usually have a story you can verify: how many years they've worked in your specific area, which neighborhoods they've built a reputation in, and whether the same family or ownership has run the business the whole time. Community reputation shows up in small ways too, like sponsoring a local youth team, showing up at a neighborhood association meeting, or having repeat customers who call them back for gutter work years after the original roof job.

A company with roots in your neighborhood has a reputation worth protecting long after the invoice is paid.

A contractor who's been local for a decade or more has already survived the scrutiny of hundreds of jobs, callbacks, and word-of-mouth referrals in the same community. Long-term accountability means they can't disappear after a bad install the way a storm chaser can, because their name and address stay put. That permanence is often the clearest signal that a company plans to be around for your warranty claim five years from now, not just for the closing signature.

Do a little homework before you assume "local" means what it claims.

Seven signs, one goal: hire a contractor who can prove what they claim instead of just saying it. Verified insurance, photo-documented assessments, honest scope-based pricing, real manufacturer backing, and a local track record aren't extras. They're the baseline for anyone trusted with the biggest system on your house. Skip that checklist and you're gambling on a roof that has to hold up through the next decade of Central Texas storms.

We built Defend Roofing around this exact list because we got tired of watching neighbors get burned by trucks that showed up after a hailstorm and vanished after the check cleared. Chris and Greyson bring three generations of roofing work to every job, backed by 100+ photo assessments and pricing you can actually read line by line. If you're comparing reputable roofers near me and want a straight answer instead of a sales pitch, reach out for a free quote and see how we stack up against that checklist yourself.