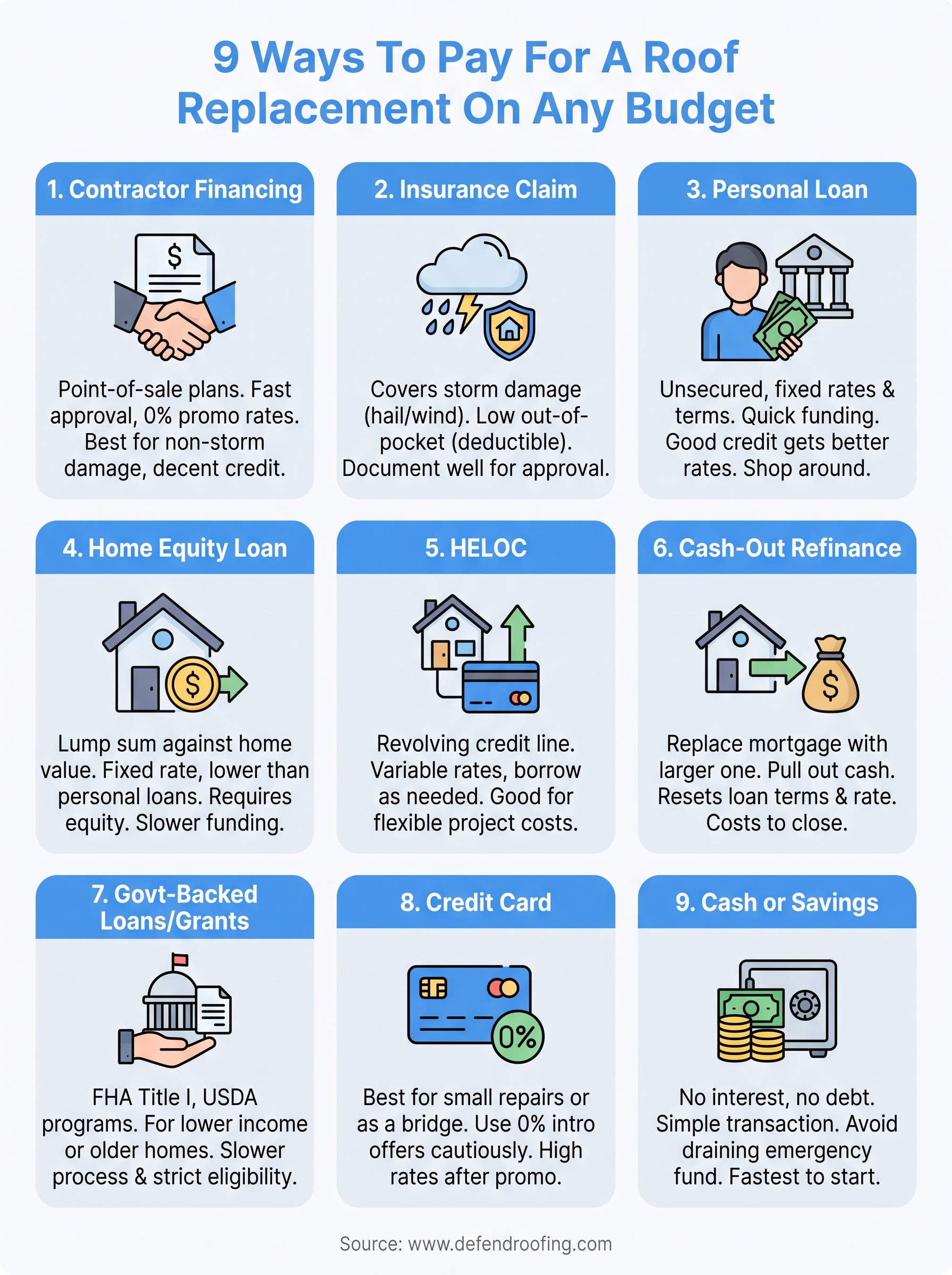

Learn how to pay for a roof replacement with 9 options—insurance, financing, HELOCs, and more—compared by cost, speed, and eligibility.

A new roof in Central Texas can run anywhere from $9,000 to $25,000 or more, and that number tends to show up right after a hailstorm, not on your own schedule. If you're wondering how to pay for a roof replacement without draining your savings or getting stuck with a loan you regret, you're not alone. Most homeowners we work with in Cedar Park, Leander, and Steiner Ranch are trying to solve this exact problem while dealing with a leak, an adjuster, or both.

The good news: you have more options than "pay cash or don't replace it." Between insurance claims, contractor financing, home equity products, and a few less obvious routes, there's usually a path that fits your situation and your credit profile.

This article walks through nine real ways to fund a roof replacement, from working an insurance claim correctly to financing plans that spread the cost over time. We'll also flag where a company like Defend Roofing's documentation-first approach, complete with 100+ photo assessments, can strengthen your claim or your loan application before you sign anything.

Many homeowners don't realize that most established roofing companies partner with third-party lenders to offer financing plans right at the point of sale. Instead of applying for a loan on your own and hoping it covers the job, you get a quote and a financing offer in the same conversation. Defend Roofing, for example, works with lenders who can approve qualified homeowners in minutes, so a $15,000 roof replacement doesn't have to come out of your checking account all at once.

Contractor financing typically runs through a partner lender rather than the roofing company itself. You fill out a short application, often online or on a tablet during your estimate, and get a decision the same day. Terms vary, but you'll usually see options like:

Since the loan is tied to the project, the contractor usually handles the paperwork alongside your estimate, which saves you from juggling a separate bank application while you're already dealing with a damaged roof.

This route suits homeowners who don't have a storm claim to fall back on, or whose claim doesn't fully cover the replacement. It's also a strong fit if you want to avoid touching your home equity or retirement savings for a repair that needs to happen now. Homeowners with fair to good credit tend to get the best promotional rates, though many lenders in this space approve a wide range of credit profiles since the loan is secured against the completed work rather than unsecured debt alone.

Contractor financing turns a five-figure roof bill into a monthly payment you can plan around, without waiting weeks for a bank's approval.

| Pros | Cons |

|---|---|

| Fast approval, often same-day | Promotional rates jump after the intro period ends |

| No separate loan shopping required | Fewer options to negotiate terms compared to a bank |

| Payments can start after project completion | Tied to a specific contractor's lender network |

| Can be combined with insurance payouts for gap coverage | Missed payments can affect your credit like any loan |

Before you sign, ask your contractor for the full rate sheet, not just the monthly payment number. A 0% intro rate that jumps to 28% APR after 12 months can turn a manageable project into an expensive one if you can't pay it off in time. A transparent contractor will walk you through the real terms and won't rush you into signing before you've compared them against at least one other financing source.

Hail and wind damage account for a huge share of roof replacements across Central Texas, and if a storm caused the damage, your homeowners insurance policy may cover most or all of the replacement cost. This is often the first option worth exploring before you consider a loan, since it can turn a $15,000 project into a few hundred dollars out of pocket, just your deductible.

After a storm, you file a claim with your insurer, who sends an adjuster to inspect the roof and estimate the damage. This is where documentation matters most. Defend Roofing's 100+ photo Precision Roof Assessment gives you evidence of the damage before the adjuster even shows up, which helps prevent a lowball estimate. Once the claim is approved, the insurer issues a payment, usually in two parts: an initial check and a final payment after the work is completed.

A well-documented claim, backed by clear photos and an honest damage assessment, is often the fastest way to a fully funded roof replacement.

This path fits homeowners whose roof damage clearly traces back to a specific storm event, hail, wind, or a fallen tree, rather than gradual wear. It's less useful if your roof is simply old and past its expected lifespan, since insurers typically deny claims tied to normal aging rather than a covered event.

| Pros | Cons |

|---|---|

| Can cover most of the replacement cost | Only applies to sudden, covered damage |

| No new debt if the payout covers the job | Claims can be denied or underpaid without documentation |

| Deductible is usually far less than the full cost | Filing a claim may raise future premiums |

| Professional inspection support strengthens your case | Adjuster timelines can delay the start of work |

Lean on a contractor who documents damage thoroughly and can speak directly with your adjuster. That kind of support closes the gap between what insurers offer and what the repair actually costs.

If your roof damage isn't storm-related and you'd rather not tie financing to a specific contractor, a personal loan from a bank, credit union, or online lender is worth a look. It's a straightforward way to borrow a fixed amount, usually $5,000 to $35,000, without putting your house up as collateral.

You apply directly with a lender, who checks your credit and income to set your rate and term. Most personal loans for home projects come with:

Once funded, the money lands in your bank account, and you pay your contractor directly, giving you full control over which roofer you hire and how the payment gets scheduled.

Homeowners with good to excellent credit get the strongest rates here, since the loan isn't backed by your home. This option suits people who want to shop multiple contractors without being locked into one lender's financing, or who don't have enough home equity built up yet for other loan types.

A personal loan gives you the freedom to choose your contractor first and worry about the payment plan second.

| Pros | Cons |

|---|---|

| No collateral risk to your home | Higher rates than secured loans |

| Funds arrive quickly, often within a week | Approval and rate depend heavily on credit score |

| Works with any contractor you choose | Smaller loan amounts than home equity options |

| Fixed payments make budgeting simple | Origination fees can reduce the amount you receive |

Compare offers from at least three lenders before committing. A half-point difference in rate on a $20,000 loan adds up fast over a five-year term.

If you've built up equity in your home and want a predictable, lower-rate way to fund a roof replacement, a home equity loan is worth serious consideration. It works like a second mortgage: you borrow a lump sum against the value of your home and pay it back over a fixed term at a fixed rate, which makes it one of the cheaper ways to cover a large roofing bill.

Lenders typically let you borrow up to 80-85% of your home's value, minus what you still owe on your primary mortgage. You receive the full amount upfront, then repay it in fixed monthly installments, usually over 5 to 20 years. Key details to expect:

Because your home secures the loan, approval depends more on your equity position than your credit score alone, though lenders still check both.

This option suits homeowners who've owned their property for several years and have meaningful equity, especially those who want a lower rate than unsecured borrowing and don't mind a slower approval process. It's a poor fit if you need funds within days, since appraisals and closing take real time.

Borrowing against your home's equity can cut your interest rate significantly, but it also means your roof and your mortgage are now linked.

| Pros | Cons |

|---|---|

| Lower rates than personal loans or cards | Your home is collateral, foreclosure risk if you default |

| Fixed payments simplify budgeting | Closing costs add to upfront expense |

| Interest may be tax-deductible for home improvements | Slower funding timeline than other options |

| Larger loan amounts available | Requires sufficient equity built up already |

Check with a tax professional about deductibility, and confirm your total equity position before applying, since a low appraisal can shrink your available loan amount.

A home equity line of credit, or HELOC, works differently from the loan you just read about. Instead of a lump sum, you get a revolving credit line secured by your home, similar to a credit card but with a much lower rate. That flexibility makes it a good fit if you're not sure exactly how much your roof replacement will cost until your contractor finishes the tear-off and finds what's underneath.

Lenders set a credit limit based on your home's equity, then you draw funds as needed during a set draw period, often 10 years, followed by a repayment period. Expect these terms:

You only pay interest on what you actually borrow, which helps if your roof job comes with unexpected add-ons like decking repair or gutter replacement.

A HELOC suits homeowners who want borrowing flexibility, maybe you're pairing a roof replacement with other projects, or you expect the final cost to shift once work begins. It's less appealing if you want payment certainty, since variable rates mean your monthly bill can rise.

A HELOC lets you borrow only what the job actually costs instead of guessing upfront and paying interest on money you didn't need.

| Pros | Cons |

|---|---|

| Borrow only what you need, when you need it | Variable rates make long-term budgeting harder |

| Lower closing costs than a home equity loan | Home serves as collateral, same foreclosure risk |

| Interest-only option eases early payments | Draw period end can trigger a payment jump |

| Reusable credit line for future projects | Requires strong equity and decent credit |

Ask your lender how rate caps work before you sign, since an uncapped variable rate can turn a manageable draw into a costly repayment period.

A cash-out refinance replaces your current mortgage with a new, larger one, and you pocket the difference in cash. If mortgage rates have dropped since you bought your home, or you've built up substantial equity, this can fund a roof replacement while resetting your loan terms at the same time. It's a bigger financial move than the options above, so it deserves a closer look before you commit.

You apply with a lender the same way you did for your original mortgage, and they qualify you based on income, credit, and your home's appraised value. Most lenders cap cash-out refinances at 80% of your home's value, which means your new loan pays off the old mortgage first, then hands you the remainder. Expect these details:

Because you're refinancing the entire mortgage, even a small rate change affects your payment on the full loan balance, not just the roofing portion.

Homeowners with substantial equity and a mortgage rate higher than current market rates get the most benefit here, since they can lower their rate and pull out cash in one move. It's a weak fit if refinancing means trading a low existing rate for a higher one just to access funds.

A cash-out refinance only makes sense if the new rate helps you, not just the roof.

| Pros | Cons |

|---|---|

| Potentially lower rate than a home equity loan | Resets your mortgage clock and total interest paid |

| One monthly payment instead of two loans | Closing costs are higher than most other options |

| Large loan amounts available | Slow process, often over a month to close |

| Fixed-rate stability throughout the term | Risky if it means giving up a lower existing rate |

Run the math with a loan officer before deciding, comparing your current rate against the new blended rate on the full balance.

If your income is limited or your home is older, a few government-backed loan programs can help fund a roof replacement at a lower cost than conventional financing. These programs exist specifically because a failing roof is a health and safety issue, not just a cosmetic one, so the federal government has built in options most homeowners never think to check.

The FHA Title I loan lets you borrow up to $25,000 for home improvements, including roofing, without home equity requirements in some cases. The USDA also offers a Section 504 Home Repair program for very low-income rural homeowners, covering repairs up to $10,000 as a loan or grant. Each program has its own application process through approved lenders or local USDA offices, and terms depend on your income, location, and the age of your home. You can find full eligibility details directly through HUD and the USDA Rural Development websites before applying.

This route suits homeowners with lower income, older homes, or rural addresses who don't qualify for large conventional loans or don't have equity to borrow against. It's a poor fit if you need funding fast, since government programs move slower than a bank or contractor lender.

Government-backed programs exist for exactly this problem, but they reward homeowners who apply early and have their paperwork ready.

| Pros | Cons |

|---|---|

| Below-market rates or partial grants | Strict income and location eligibility |

| Designed specifically for home repairs | Slower approval than private lenders |

| Some rural grants don't require repayment | Loan caps may not cover a full replacement |

| Backed by federal agencies, added stability | More paperwork than conventional financing |

Start with your local USDA office or an FHA-approved lender, and apply well before your roof reaches emergency status, since these programs rarely move fast enough for an active leak.

For a smaller repair or a roof patch under a few thousand dollars, a credit card can be the fastest way to cover the bill, especially if you already have a card with a decent limit sitting unused. It's rarely the cheapest way to fund a full roof replacement, but for quick jobs or as a stopgap while other financing clears, it has a real place in the lineup of options for how to pay for a roof replacement.

You simply hand your contractor a card, or pay through an online invoice, and the charge hits your existing credit line. Some homeowners open a new card specifically for the project to take advantage of a 0% introductory APR offer, often lasting 12 to 21 months. Others rely on rewards cards to earn cash back or points on a large purchase, treating the roof bill like any other expense.

A credit card can bridge a gap fast, but the interest that kicks in after the promo period can undo any savings you thought you locked in.

This option fits homeowners tackling a repair rather than a full tear-off, or those who can pay off the balance within a promotional window. It also works as a short-term bridge while waiting on an insurance payout or a loan to fund, rather than as the primary way to cover a $15,000 replacement.

| Pros | Cons |

|---|---|

| Instant access, no application wait | High standard APRs, often 20% or more |

| Rewards or cash back on the purchase | Can hurt your credit utilization ratio |

| Good for small repairs or deposits | Not practical for full replacements |

| 0% intro offers help if paid off fast | Interest resets to full rate if balance lingers |

Only lean on a card if you have a realistic plan to pay it off before the promotional rate expires.

Paying with cash or savings is the simplest way to fund a roof replacement, and it's the only option on this list that doesn't involve interest, credit checks, or a lender of any kind. If you've built up an emergency fund or a dedicated home repair account, writing a check for the full project cost means you own the roof outright the day the crew finishes cleanup, with no monthly payment following you afterward.

There's no application here, just a straightforward transaction between you and your contractor. Most roofers, including Defend Roofing, structure cash payments in stages tied to project milestones:

Splitting payments this way protects you from paying in full before the work is done, and it gives you a natural checkpoint to review the job before releasing the last payment.

Cash makes the most sense for homeowners who've planned ahead, whether through a house maintenance fund, a recent bonus, or savings earmarked specifically for this kind of repair. It's a weaker choice if paying cash would wipe out your emergency reserves, since an unexpected expense right after a big cash outlay can leave you exposed.

Paying cash costs you nothing in interest, but only if it doesn't cost you your financial cushion.

| Pros | Cons |

|---|---|

| No interest, fees, or credit impact | Ties up a large lump sum at once |

| Full ownership with no lender involved | Can drain savings meant for emergencies |

| Often gives leverage to negotiate price | Opportunity cost of not investing that cash |

| Fastest path to starting the project | Not realistic for most five-figure jobs |

If you can pay cash without touching your safety net, it's the cleanest option on this list. If it means borrowing from your emergency fund to rebuild later, one of the financing routes above may leave you in better shape.

No single option on this list is the right answer for every homeowner. Storm damage points you toward an insurance claim first, strong equity points you toward a home equity loan or HELOC, and a tight timeline with decent credit points you toward contractor financing or a personal loan. The real work is matching your situation, your credit, your equity, and how fast you need the roof done, to the option that costs you the least over time, not just the smallest number today.

Whatever route you choose, start with an honest assessment of the roof itself. A documented, photo-backed inspection tells you whether you're financing a repair or a full roof replacement, and that answer changes which payment option actually makes sense. If you're in Cedar Park, Leander, Steiner Ranch, or anywhere else in Central Texas, get in touch with Defend Roofing for a straightforward quote and a clear picture of what your project really costs.