Does homeowners insurance cover roof replacement? Learn to distinguish storm damage from wear, understand your policy, and document proof for your claim.

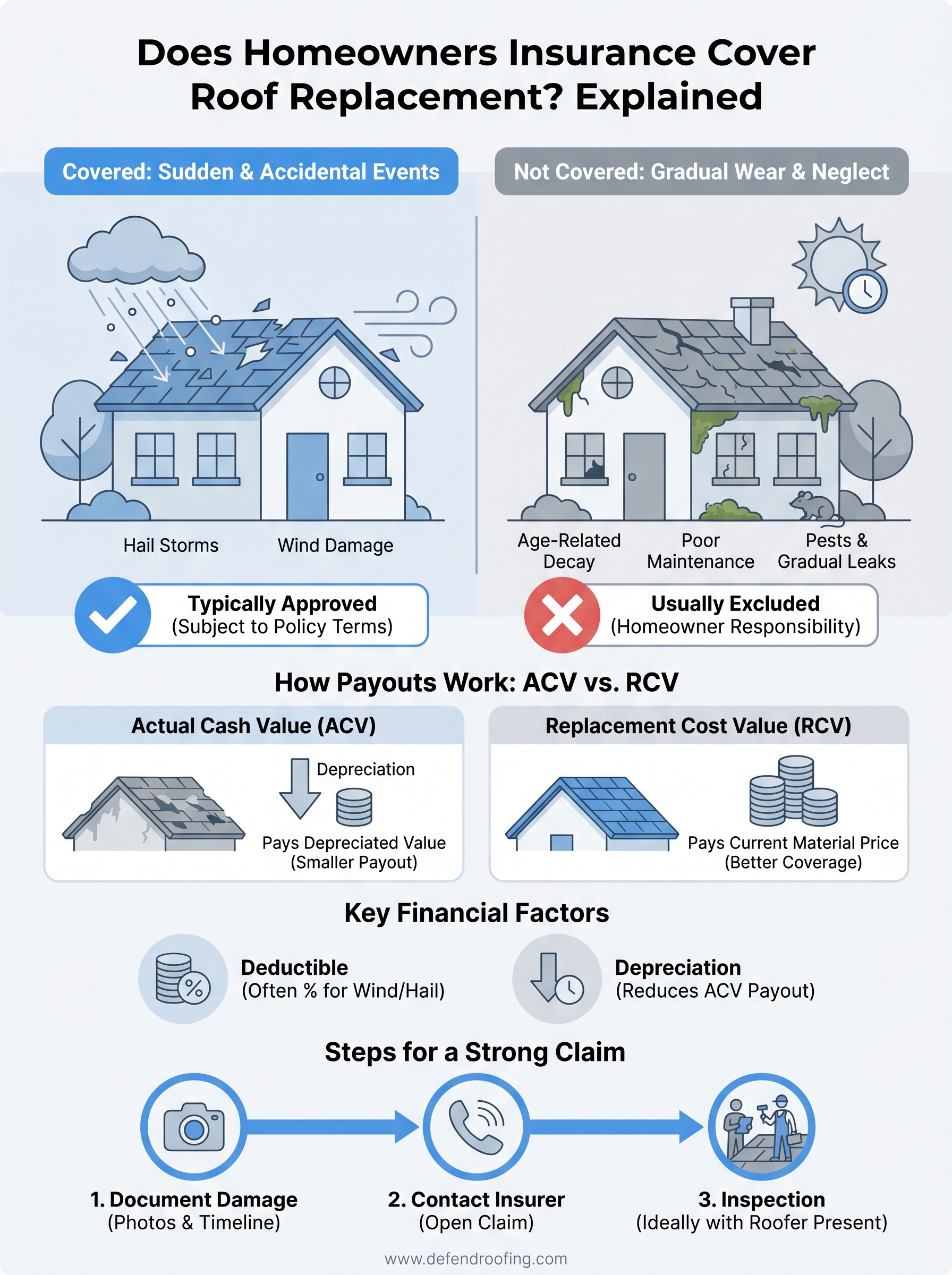

Your roof takes a hit during a storm, and the first question that crosses your mind is: does homeowners insurance cover roof replacement? The short answer is, it depends. Insurance typically covers roof damage caused by sudden, unexpected events like hail or wind, but it won't pay for a roof that's simply worn out from age or neglect.

That distinction matters more than most homeowners realize, and it's one we walk families through regularly at Defend Roofing. As a family-owned roofing contractor serving Central Texas, we've helped hundreds of Austin-area homeowners assess storm damage, document their roof's condition with 100+ photos, and navigate the insurance claim process from first call to final check. We've seen claims approved and claims denied, and the difference usually comes down to understanding what your policy actually covers before you file.

This article breaks down when insurance pays for a roof replacement, what's typically excluded, and what steps you can take to give your claim the strongest possible foundation.

Most homeowners assume their policy covers roof damage the same way it covers a burst pipe or a fire, but roofing coverage works differently. The core issue is that insurance is designed to cover sudden, accidental events, not the slow breakdown of materials over time. When a claim gets denied, it's almost always because the damage falls on the wrong side of that line.

When you ask whether does homeowners insurance cover roof replacement, the answer hinges on how the damage started. A hailstorm that punches through your shingles in an afternoon qualifies as a covered peril under most standard policies. A roof that's been slowly losing granules for five years does not. The problem is that many roofs show both types of damage at the same time, which makes it genuinely hard for homeowners to know how an adjuster will view their claim.

Insurance adjusters are trained to look for pre-existing deterioration, and they will document it, even when a real storm event caused additional damage on top of it.

Your roof's age also plays a direct role. Many insurers apply actual cash value (ACV) calculations that factor in depreciation, meaning a 15-year-old roof may only receive a fraction of the full replacement cost even when storm damage is legitimate and clearly documented.

Standard homeowners policies use broad terms like "sudden and accidental" without always defining what that means for roofing materials specifically. Two neighbors on the same street, with the same storm damage, can get different outcomes based on their specific policy language, their insurer's internal guidelines, and how thoroughly the damage was documented at the time of inspection. Reading your policy carefully before you file, not after, puts you in a much stronger position.

When your insurer approves a roof claim, the payout method your policy uses determines how much you actually receive. Most policies use either actual cash value (ACV) or replacement cost value (RCV), and that distinction has a real effect on your final check.

Actual cash value factors in depreciation, so an older roof produces a smaller payout. A 12-year-old roof that costs $15,000 to replace might only generate a $6,000 ACV check after depreciation is applied. Replacement cost value policies pay based on current material prices, covering far more of the actual replacement expense.

Knowing your policy type before a storm hits answers a key part of whether does homeowners insurance cover roof replacement at a level that actually solves the problem.

Insurers typically send payment in two rounds: an initial check after claim approval, then a second check once the completed work is verified. Your mortgage lender may appear on the payment, which adds an extra step before you can access the funds.

Understanding exclusions is just as important as knowing what's covered. Most standard policies draw a hard line around age-related deterioration and poor maintenance, treating these as the homeowner's responsibility rather than an insurable event.

If your roof has been slowly losing granules, showing cracked or curling shingles, or developing moss growth over several years, your insurer will likely classify that as normal wear and tear. Filing a claim for gradual deterioration is one of the fastest ways to get a denial. When you ask does homeowners insurance cover roof replacement, the honest answer for an aging, unmaintained roof is almost always no.

A well-documented maintenance history can protect you from having legitimate storm damage dismissed as pre-existing neglect.

Most policies explicitly exclude the following from coverage:

Knowing these specific exclusions before you file keeps you from spending time on a claim that has no realistic path to approval.

Getting a roof claim right comes down to preparation and documentation. The steps you take in the first 24 to 48 hours after a storm can determine whether your insurer treats your claim as solid evidence or a vague request they can push back on.

Your first move is to photograph every inch of visible damage from the ground and, if safe, from the roof itself. Note the date of the storm, collect weather reports that confirm the event, and write down when you first noticed the problem. This creates a timeline your insurer cannot easily dispute.

If you're asking does homeowners insurance cover roof replacement after a recent storm, your documentation is the single biggest factor in getting a fair answer.

Call your insurance company promptly to open a formal claim. When the adjuster visits, have a qualified roofer present to point out damage the adjuster might miss and ensure the full scope gets recorded.

Three financial factors shape how much money you actually walk away with after a claim: your deductible, depreciation, and any endorsements attached to your policy. Understanding each one before you file gives you a realistic picture of your out-of-pocket costs.

Many policies carry a separate wind and hail deductible calculated as a percentage of your home's insured value rather than a flat dollar amount. On a $350,000 home with a 2% hail deductible, you owe $7,000 before your insurer pays anything, which changes the math on whether filing makes financial sense at all.

When you ask does homeowners insurance cover roof replacement, knowing your deductible type upfront prevents major surprises after the claim is approved.

Some insurers offer optional endorsements that can significantly improve your coverage terms. Two of the most useful ones are:

Adding the right endorsement before a storm hits costs far less than absorbing a large depreciation deduction after one.

Now you have a clear picture of when does homeowners insurance cover roof replacement and when it does not. The difference between a paid claim and a denied one usually comes down to the cause of damage, your policy type, and how thoroughly you documented the problem from the start.

If a recent storm hit your home, or you simply want to know the true condition of your roof before trouble starts, the right move is a professional inspection with detailed photo documentation. At Defend Roofing, we provide every homeowner with a 100+ photo Precision Roof Assessment that gives you honest answers and adjuster-ready evidence, no pressure, no upselling.

Chris and Greyson are ready to walk the roof with you and give you a straight answer about what your roof actually needs. Schedule your free roof assessment today and get the documentation your claim depends on.