Wondering can you finance a roof replacement? Compare 8 options—loans, HELOCs, insurance & more—to find the best fit for your budget.

A new roof in Central Texas runs anywhere from $9,000 to $20,000 or more, and most homeowners don't have that sitting in a savings account. So the question comes up fast: can you finance a roof replacement without draining your reserves or settling for a contractor who cuts corners to hit your budget? Yes, you can, and you have more choices than you probably think.

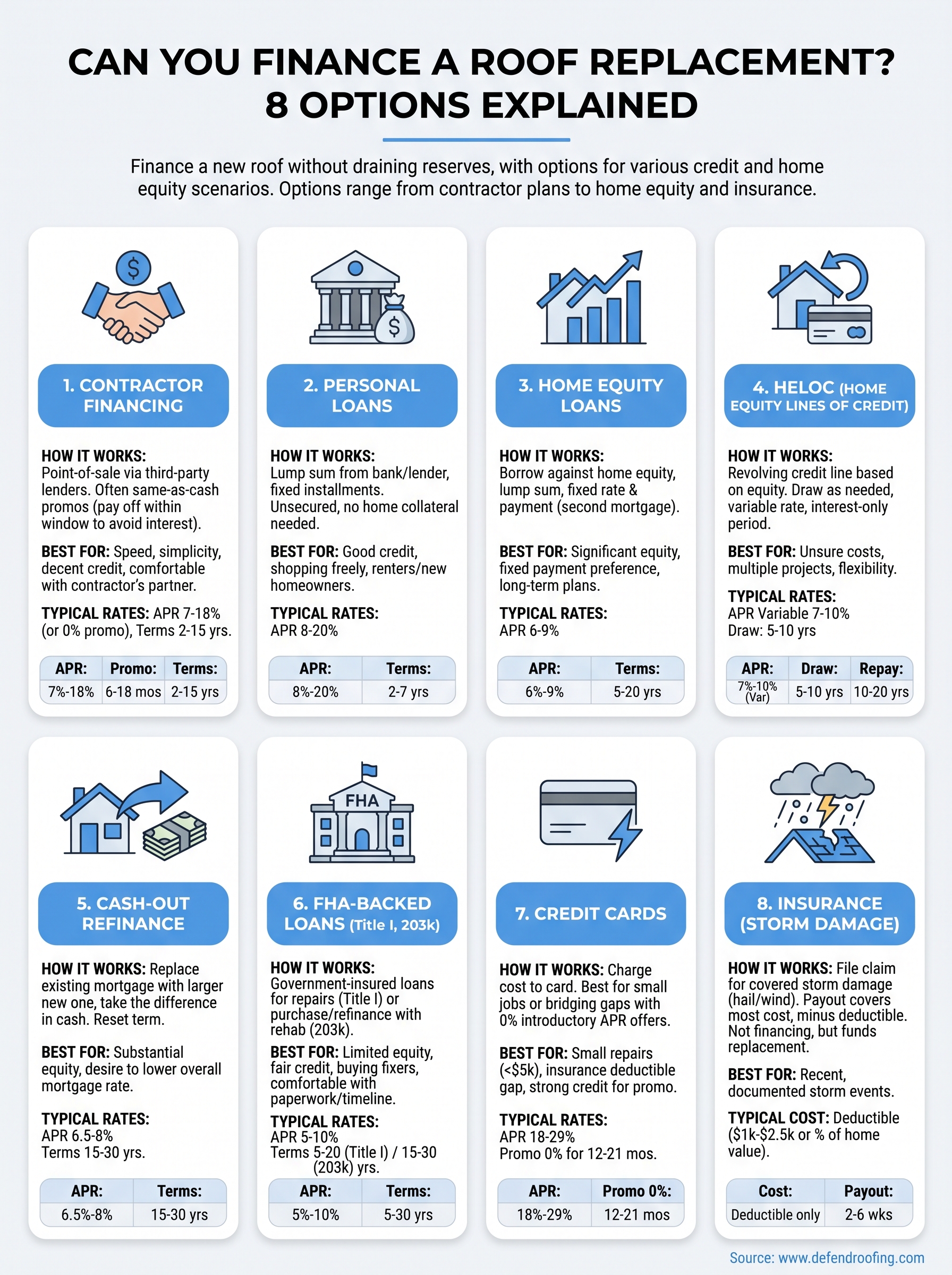

The short answer is that financing a roof is common, and lenders, contractors, and even your own insurance policy offer different paths depending on your credit and situation. Options range from contractor financing plans with same-as-cash promotions to home equity loans, personal loans, and credit cards for smaller jobs. Your credit score matters, but it doesn't have to be perfect to qualify for something workable.

Below, we break down eight real financing options, what they cost, who qualifies, and how to match one to your specific circumstances, whether you're dealing with storm damage, an aging roof, or just planning ahead before a leak turns into a bigger problem.

Many roofing companies, including Defend Roofing, partner with third-party lenders to offer financing right at the point of sale. Instead of applying for a loan on your own and waiting days for approval, you fill out an application during your estimate appointment and often get a decision in minutes. This is usually the fastest route from roof inspection to signed contract, which matters if you're dealing with an active leak or storm damage that's getting worse by the week.

When a roofing contractor offers financing, they're not lending you money themselves. They've set up a relationship with a lending partner, similar to how a furniture store or car dealership works with banks. You apply through a simple form, usually online or on a tablet during your in-home consultation, and the lender runs a soft or hard credit check depending on the program. Approved amounts typically cover the full project cost, and funds get paid directly to the contractor once the job is done or at agreed milestones.

Same-as-cash promotions are common in this space, meaning you pay no interest if you pay off the balance within a promotional window, often 12 to 18 months. Miss that deadline, though, and some plans apply retroactive interest to the entire original balance, not just what's left. Read the terms carefully before you sign.

Contractor financing suits homeowners who want speed and simplicity over shopping multiple lenders. It works well if:

This option is less ideal if your credit is weak, since contractor lending partners tend to have tighter approval standards than personal loan marketplaces with more flexible underwriting.

| Feature | Typical Range |

|---|---|

| APR (standard plans) | 7% to 18% |

| Same-as-cash promo period | 6 to 18 months |

| Loan terms | 2 to 15 years |

| Credit score needed | 620+ for most programs |

| Funding speed | Same day to a few days |

Rates vary widely based on the lending partner and your credit profile. A homeowner with a 750 credit score might land a 7% APR, while someone in the mid-600s could see rates closer to 18%, which starts to resemble credit card pricing.

The biggest advantage is convenience. You're not filling out separate applications, waiting on multiple approvals, or coordinating disbursement timing between a lender and a contractor. The same-as-cash structure also gives disciplined borrowers a genuine interest-free financing window if they pay it off on schedule.

Contractor financing trades convenience for less negotiating power, so read the promotional terms before you sign anything.

On the downside, you're often locked into whatever lending partner your contractor works with, which means less room to shop for a better rate elsewhere. Retroactive interest clauses on same-as-cash deals catch people off guard, and if you don't pay attention to the payoff date, a $15,000 roof can suddenly accrue a year's worth of deferred interest all at once. It's also worth asking your contractor upfront whether they mark up project pricing to offset dealer fees paid to the lender, since that's a common practice in home improvement financing across the industry, not just roofing. A reputable contractor should answer that question directly without hesitation.

Personal loans give you a lump sum from a bank, credit union, or online lender that you repay in fixed monthly installments, completely separate from your roofing contractor. This option makes sense if you want to control the financing side yourself and negotiate roof pricing without a lender attached to the deal. Since the loan is unsecured, you don't put your house up as collateral, which appeals to homeowners who'd rather not touch their home equity for a repair.

You apply directly with a lender, either online or in person, and most decisions come back within a day or two. Approval depends on your credit score, income, and existing debt load rather than the value of your home. Once approved, the lender deposits funds into your bank account, and you pay the contractor yourself, on your own schedule, using whatever payment method the contract calls for.

Personal loans work well for a specific type of borrower:

If your credit sits below the mid-600s, expect either denial or a rate that makes this option less attractive than others on this list.

| Feature | Typical Range |

|---|---|

| APR | 8% to 20% |

| Loan terms | 2 to 7 years |

| Credit score needed | 640+ for competitive rates |

| Funding speed | 1 to 3 business days |

The Consumer Financial Protection Bureau notes that personal loan rates vary significantly by lender, so comparing at least three offers before committing is worth the extra hour it takes.

Speed and flexibility are the main draws here. You get cash fast, you're not restricted to one contractor's financing partner, and there's no risk to your home if payments get tight.

A personal loan keeps your house out of the deal, but you'll pay for that safety with a higher interest rate than home equity options.

The tradeoff is cost. Unsecured rates run higher than home equity products, and a poor credit profile can price you out of a reasonable APR altogether.

A home equity loan lets you borrow against the value you've built up in your house, paid out as a lump sum with a fixed rate and fixed monthly payment. Homeowners often call this a second mortgage, since it sits on top of your existing loan and uses your property as collateral. For a roof replacement that runs $15,000 or more, this option often beats a personal loan on rate, though it comes with more paperwork and a slower timeline.

You apply through a bank, credit union, or online lender, and they order an appraisal or use an automated valuation to figure out your home's current worth. Subtract what you still owe on your mortgage, and the difference is roughly how much equity you have available to borrow against, usually up to 80% to 85% of that combined loan-to-value limit. Once approved, you receive the full amount in one deposit and start repaying it in fixed installments, separate from your primary mortgage payment.

This financing route fits homeowners who've owned their property for several years and built meaningful equity, especially in markets like Cedar Park or Steiner Ranch where home values have climbed steadily. It suits people who want a predictable payment and plan to stay in the home long enough to pay off the loan comfortably. It's a poor fit if you bought recently with a small down payment, since you likely won't have enough equity to tap yet.

| Feature | Typical Range |

|---|---|

| APR | 6% to 9% |

| Loan terms | 5 to 20 years |

| Credit score needed | 680+ for best rates |

| Funding speed | 2 to 6 weeks |

Rates on home equity loans track closely with your credit score and combined loan-to-value ratio, and they typically beat unsecured personal loans by several percentage points.

The rate is the main selling point. Fixed payments make budgeting simple, and interest may be tax-deductible if the funds go toward home improvements, though you should confirm that with a tax professional since rules changed under the IRS after 2017 tax reform.

A home equity loan trades a lower rate for real risk, since your house backs the debt if payments stop.

The downside is obvious: your home secures the loan, so missed payments put your property at risk. Closing costs and appraisal fees also add time and expense that faster options skip entirely.

A home equity line of credit, or HELOC, works more like a credit card secured by your house than a traditional loan. Instead of receiving one lump sum, you get a credit limit you can draw from as needed during a set draw period, which suits a roof project that might expand once your contractor gets a closer look at the decking or flashing. Defend Roofing's 100+ photo assessments often reveal secondary issues, like rotted sheathing, that add cost mid-project, and a HELOC gives you room to cover that without applying for a second loan.

Lenders approve you for a maximum credit line based on your home's equity, then let you draw funds as you need them, typically over a 5 to 10 year draw period. During that time you often make interest-only payments on whatever balance you've pulled. Once the draw period ends, the line converts to a repayment period, usually 10 to 20 years, where you pay down both principal and interest on a fixed schedule.

Homeowners who aren't sure of the final project cost benefit most, since a HELOC lets you draw only what you use rather than borrowing a fixed amount upfront. It also fits people planning multiple home projects over a few years, using the same line for a roof now and gutters or siding later. Steady equity and a credit score above 680 make approval and pricing easier.

| Feature | Typical Range |

|---|---|

| APR | Variable, 7% to 10% |

| Draw period | 5 to 10 years |

| Repayment period | 10 to 20 years |

| Credit score needed | 680+ for best rates |

| Funding speed | 2 to 6 weeks |

Most HELOCs carry a variable rate tied to the prime rate, so your payment can shift as broader interest rates move, unlike the fixed payment on a home equity loan.

Flexibility is the clear advantage. You only pay interest on funds you actually draw, which keeps costs down if the roof job comes in under estimate.

A HELOC gives you flexible access to funds, but a variable rate means your payment isn't fixed for the life of the loan.

The downside is unpredictability. Rate increases can raise your payment without warning, and like a home equity loan, your house secures the debt, so missed payments carry real consequences.

A cash-out refinance replaces your existing mortgage with a new, larger one and hands you the difference in cash. If you've owned your home for a while and rates have moved in your favor since you bought, this option lets you fund a roof replacement while potentially restructuring your whole mortgage at the same time. It's the most involved financing route on this list, but it can also carry the lowest rate since it's secured by a first-position mortgage rather than a second loan sitting behind it.

You apply with a mortgage lender, who orders a new appraisal and evaluates your income, debt, and credit just like a purchase mortgage. The new loan pays off your current mortgage balance, and you pocket the remaining equity in cash, up to typically 80% of your home's appraised value. Closing looks a lot like buying a house: inspections, title work, and a stack of paperwork, often taking 30 to 45 days from application to funding.

This option fits homeowners who already have substantial equity and either want a lower mortgage rate than they currently have or don't mind resetting their loan term for the sake of accessing cash at scale. It works less well if your current mortgage rate is already low, since refinancing into a higher rate to fund a roof can cost you more over time than a smaller, separate home equity loan would.

| Feature | Typical Range |

|---|---|

| APR | 6.5% to 8% |

| Loan terms | 15 to 30 years |

| Credit score needed | 620+ (680+ for best pricing) |

| Funding speed | 30 to 45 days |

Rates track general mortgage market conditions, and the Consumer Financial Protection Bureau advises comparing at least three lenders since closing costs and fees vary widely on refinances.

Long repayment terms spread the roof's cost over decades, keeping monthly payments low compared to shorter-term loans. Combining a rate reset with roof funding can also make financial sense if market rates have dropped since your original purchase.

A cash-out refinance can lower your overall borrowing cost, but resetting your mortgage clock means paying interest on your home for longer.

Closing costs run 2% to 5% of the loan amount, and stretching a roof repair over 30 years means you'll pay far more in total interest than a shorter-term product would.

The FHA Title I loan program and the 203(k) rehabilitation mortgage both let homeowners finance roof work through government-backed lending, even with credit that wouldn't qualify for the best conventional rates. These programs come through the Federal Housing Administration, which insures the loan rather than issuing it directly, so you still work with a regular bank or approved lender for the application.

Title I loans work for smaller repairs, up to $25,000 on a single-family home, and don't always require equity since some lenders offer unsecured versions under $7,500. A 203(k) loan, by contrast, wraps roof replacement costs into a home purchase or refinance mortgage, useful if you're buying a fixer-upper or refinancing a home that needs a new roof alongside other repairs. Either way, the lender submits paperwork to HUD for approval, and funds often get released in draws tied to inspection milestones rather than one lump payment.

These loans suit a narrower slice of homeowners than the options above:

If you already own your home outright and just need a straightforward repair loan, this route usually adds more complexity than it's worth.

| Feature | Typical Range |

|---|---|

| APR | 5% to 10% |

| Loan terms | 5 to 20 years (Title I); 15 to 30 years (203k) |

| Credit score needed | 580+ for many lenders |

| Funding speed | 3 to 8 weeks |

Rates run competitive with home equity products, but the approval process takes longer because of HUD's involvement and inspection requirements.

FHA-backed loans open doors for buyers and lower-credit homeowners, but the paperwork and timeline rule out anyone needing a fast fix.

Lower credit thresholds make this option accessible to homeowners shut out of conventional lending, and rates stay reasonable compared to unsecured products. The tradeoff is speed and simplicity: draw-based disbursements, HUD paperwork, and lender-specific overlays stretch the timeline well past what a personal loan or contractor financing plan would take, so it's not the right fit for an active leak.

Credit cards work best for smaller roof jobs or as a backup source of funds when other financing falls through. Using a card to cover a full roof replacement is possible, but the math rarely works in your favor unless you qualify for a 0% introductory APR card and can pay off the balance before that promotional rate expires. For patch repairs, deductibles, or the gap between an insurance payout and total project cost, though, a card can be the simplest tool you already have.

You charge the roofing cost directly to your card, either paying the full contractor invoice at once or splitting payments across a project timeline if your contractor accepts partial charges. Some cards offer promotional 0% financing for 12 to 21 months on purchases, which functions similarly to a same-as-cash plan, minus any application process since you're using an account you already have open.

Credit cards suit homeowners tackling repairs under $5,000, or anyone bridging a short-term cash gap while waiting on insurance reimbursement. They also work for people with strong credit who can secure a long 0% promo window and discipline themselves to pay it off on schedule.

| Feature | Typical Range |

|---|---|

| Standard APR | 18% to 29% |

| Promotional 0% APR period | 12 to 21 months |

| Credit score needed | 690+ for best promo offers |

| Funding speed | Immediate |

Once a promotional period ends, remaining balances jump to the card's standard rate, which the Consumer Financial Protection Bureau flags as one of the most expensive forms of consumer debt available.

Instant access is the clear benefit here. There's no application delay, no appraisal, and no waiting on a lender's decision, since you're using credit you already have.

A credit card can cover a small roof repair fast, but carrying a large balance past the promo window turns a manageable bill into an expensive one.

The downside shows up the moment the promotional rate expires. Standard interest rates on cards routinely exceed 20%, turning a $10,000 roof into a debt that grows faster than most homeowners expect if they only make minimum payments.

Insurance isn't technically financing, but for hail and wind damage in Central Texas, it's often the fastest way to cover a roof replacement without touching your savings or taking on debt at all. If a covered storm caused the damage, your policy may pay for most or all of the replacement cost, minus your deductible. This is frequently the first place homeowners should look before asking can you finance a roof replacement through a loan, since a legitimate claim can eliminate the need for financing altogether.

You file a claim with your insurer, who sends an adjuster to inspect the roof and document damage. Documentation matters here, which is why Defend Roofing's 100+ photo assessments help homeowners build a case before the adjuster even arrives. If the adjuster agrees the damage is storm-related and covered under your policy, the insurer issues a payment, usually in two parts: an initial payment and a final one released once the work is done, matching your policy's actual cash value and replacement cost provisions.

This route fits homeowners who've had a recent hailstorm or wind event and can point to a specific date of loss. It works best when the roof shows clear, adjuster-visible damage rather than gradual wear from age, which most policies exclude entirely.

| Feature | Typical Range |

|---|---|

| Deductible | $1,000 to $2,500 (or 1% to 2% of home value) |

| Claim payout timeline | 2 to 6 weeks |

| Coverage type needed | Replacement cost, not just actual cash value |

Covered claims can fund most of the replacement without a loan, leaving you responsible for just the deductible. Getting a detailed damage assessment from your roofer before filing strengthens your position with the adjuster and helps prevent a lowball settlement.

A well-documented claim can turn a five-figure roof bill into a single deductible payment, but only if the damage is genuinely storm-related.

The downside is that insurance only applies to covered events, not routine aging or neglect, and disputed claims can drag on for months, leaving you needing a backup financing plan in the meantime.

Sorting through eight options is only useful if you can quickly match one to your actual situation. Start with the question that decides everything else: is this an emergency repair or a planned replacement? A leaking roof after a storm points you toward contractor financing or a fast personal loan, while a roof you know is aging out over the next year gives you time to shop home equity products or wait on a HELOC approval.

Your credit score narrows the field almost immediately. Below 620, expect FHA-backed loans or contractor programs with higher rates to be your realistic paths, since conventional home equity products and the best personal loan rates typically require 680 or above. Above 700, you gain access to nearly everything on this list, which means the decision shifts from "what can I qualify for" to "what costs the least over time."

Equity matters just as much as credit. If you've owned your home for years and have significant equity built up, home equity loans and HELOCs almost always beat unsecured options on rate. If you're a newer homeowner without much equity yet, personal loans or contractor financing become your default, since there's nothing to borrow against.

Run through this checklist before picking:

The right financing choice isn't the cheapest one on paper, it's the one that fits your timeline, your equity, and your tolerance for risk.

Often the smartest move is combining approaches. File an insurance claim first if storm damage applies, then use a short-term personal loan or contractor plan to cover the deductible gap. Answering can you finance a roof replacement really means answering these smaller questions first, and the right combination usually reveals itself once you do.

Before you decide how to finance a roof, it helps to know why one estimate lands at $9,000 and another for a similar-sized house hits $22,000. Roof size and pitch account for the biggest swing. A steep roof takes longer to work on safely, requires more scaffolding and harnesses, and slows down every crew on the job, which adds labor cost even if the square footage matches a flatter roof down the street.

Material choice moves the number just as much. Standard architectural shingles remain the most affordable option in Central Texas, while metal roofing, tile, or impact-resistant shingles designed to hold up against hail push the price up considerably. Impact-resistant materials often qualify for an insurance premium discount, though, so the higher upfront cost sometimes pays for itself over a few years if your carrier offers that credit.

What's underneath the shingles matters too. Defend Roofing's 100+ photo assessments regularly turn up rotted decking, damaged flashing, or inadequate ventilation that wasn't visible from the ground. Replacing plywood sheathing or upgrading attic ventilation adds real cost, but skipping that work to save money now typically leads to a shorter roof lifespan and a bigger bill later.

The roof you can see is rarely the whole story, and what's underneath often decides whether your project stays on budget.

Here's a quick breakdown of what typically moves the price:

| Cost Driver | Impact on Price |

|---|---|

| Roof size (squares) | Direct, largest single factor |

| Pitch/steepness | Adds labor cost and time |

| Material (shingle vs. metal vs. tile) | Can double the price per square |

| Decking or structural repairs | Adds $50 to $150 per sheet replaced |

| Number of layers to remove | Adds tear-off labor cost |

| Ventilation and flashing upgrades | Smaller cost, improves longevity |

Local permitting fees and disposal costs round out the estimate, and both vary by city within the Austin area. Getting a detailed, itemized quote rather than a flat number lets you see exactly which of these factors is driving your specific price, and it gives you a clearer picture of how much financing you'll actually need before you commit to a loan or a line of credit.

Homeowners researching financing tend to circle back to the same handful of questions, so let's clear those up directly.

Yes, though your options narrow. FHA Title I loans and some contractor financing programs accept scores as low as 580, and a co-signer with stronger credit can improve your terms on a personal loan. Rates will run higher than what a 720-credit-score homeowner sees, but a roof replacement rarely waits for your credit to improve, so a workable option usually exists even at the lower end.

Only if the damage stems from a covered event like hail or wind, not general aging. Storm-related claims typically cover most of the replacement cost minus your deductible, while a roof that's simply old and worn gets no help from your policy at all.

Insurance pays for sudden damage, not the slow wear every roof experiences over time.

Lenders look at your income, existing debt, and either your credit score or home equity, depending on the loan type. A debt-to-income ratio under 43% keeps most doors open, while home equity loans and HELOCs cap borrowing around 80% to 85% of your combined loan-to-value.

That depends on your opportunity cost. If a 0% promotional financing plan is available and you'd otherwise earn more parking that cash in savings or investments, financing makes sense even with money in the bank. If every option on the table charges real interest, paying cash saves you money outright.

Absolutely, and it's common. Homeowners frequently use a partial insurance payment to cover most of the job, then finance the deductible or any upgrade costs, like impact-resistant shingles, that fall outside the policy's coverage. This keeps the loan amount small and manageable rather than financing the entire project.

So yes, you can finance a roof replacement, and you have real options at nearly every credit level and equity situation. Contractor financing gets you moving fast, home equity products often win on rate, and a legitimate storm claim can wipe out most of the bill before financing even enters the picture. None of these choices is universally right, but one of them fits your timeline, your credit, and your risk tolerance better than the rest.

The next step isn't picking a lender first. It's getting an honest, itemized quote so you know exactly how much you actually need to finance. Guessing at a number leads to over-borrowing or coming up short mid-project. Defend Roofing builds every estimate on a 100+ photo assessment, so you're financing the real scope of work, not a rough estimate. Get in touch for your instant quote and start with numbers you can trust.