Does homeowners insurance cover roof damage? Learn what's covered, deductibles, claim deadlines, and how to document hail damage in Central Texas.

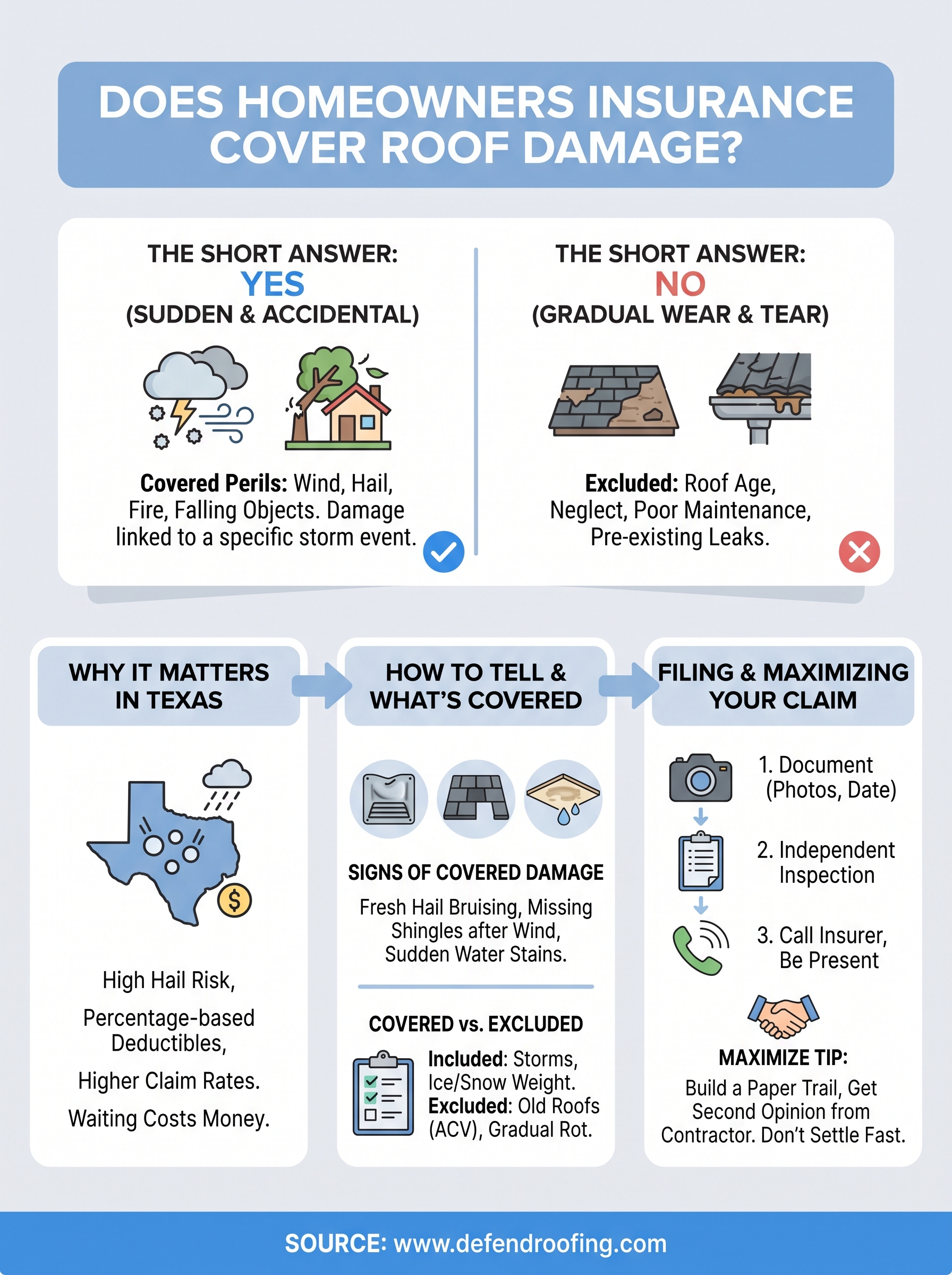

You hear a hard hail storm roll through Cedar Park or Leander, and the first question you ask isn't about the noise on the roof. It's whether your policy will actually pay for the damage. So does homeowners insurance cover roof damage? The short answer is yes, in many cases, but only when the cause is sudden and accidental, not the result of age or neglect.

Insurance companies draw a hard line between sudden, covered perils like hail, wind, and fallen trees, and gradual deterioration like worn shingles or long-term wear. That distinction decides whether your claim gets approved or denied, and adjusters look closely for evidence one way or the other. Understanding that line before you file a claim puts you in a much stronger position.

In this article, we break down exactly what's typically included in a standard policy, what usually gets excluded, and how factors like your roof's age and material affect your payout. We'll also cover what documentation strengthens your claim, since that's where detailed damage evidence and a thorough inspection make the biggest difference between a fair settlement and a fight with your insurer.

Central Texas sits squarely in one of the country's most active hail corridors, and that reality shapes how seriously you should take your policy's roof coverage. Austin-area homeowners file storm-related roof claims at a rate far higher than the national average, and insurers know it. That's why so many Texas policies now carry separate wind and hail deductibles, often calculated as a percentage of your home's insured value rather than a flat dollar amount.

Hail season in Texas typically runs from March through June, but severe thunderstorms and straight-line winds can bring damage almost any month. A single hailstorm can leave thousands of homes in Cedar Park, Avery Ranch, or Leander with cracked shingles and dented flashing within minutes.

| Risk Factor | Why It Matters in Central Texas |

|---|---|

| Hail frequency | Among the highest in the US, concentrated in spring months |

| Roof age | Older roofs show more granule loss, weakening hail resistance |

| Deductible structure | Many policies use percentage-based wind/hail deductibles |

| Claim timing | Delayed reporting can shrink or void your payout |

In Central Texas, your roof's insurance coverage isn't a formality, it's the financial buffer between you and a five-figure repair bill.

Understanding your coverage before a storm hits, not after, gives you leverage. Homeowners who wait to review their policy often discover exclusions or coverage gaps only after they've already filed, when it's too late to adjust. Knowing your deductible structure and coverage limits ahead of time means you can act fast and confidently when a Texas storm rolls through.

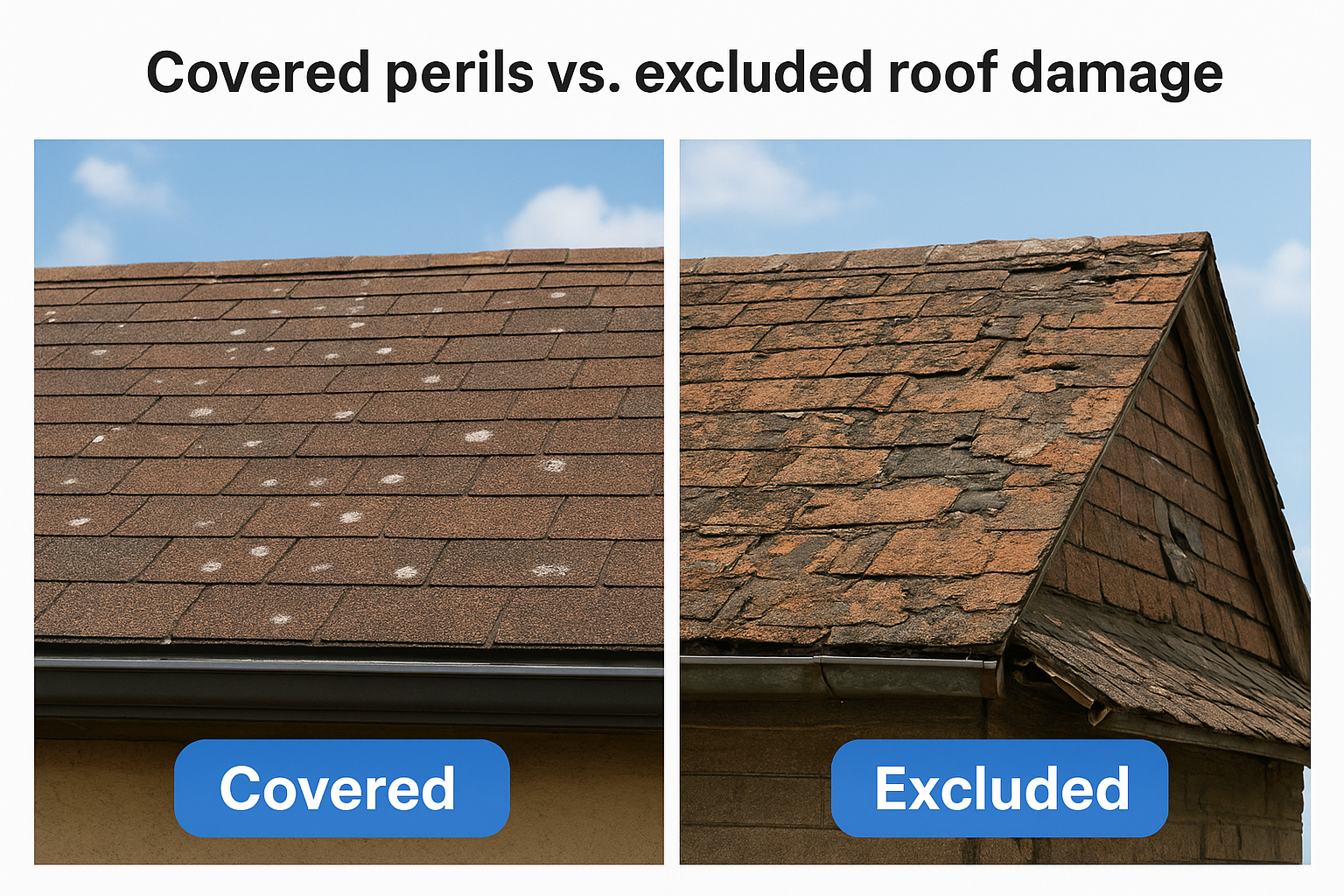

Before you call your insurer, walk your property and look for specific clues that point to a sudden event rather than gradual wear. Hail dents on soft metal like gutters, vents, or AC units often mean hail also hit your shingles. Missing shingles after a windstorm, a fresh tree limb on the roof, or granules piling up in your gutters right after a storm all suggest storm-related damage that's likely covered.

Check for these before you contact your adjuster:

If the damage traces back to one specific storm date, you're in far better shape than if it's spread out over years.

Document everything with photos and note the date of the storm that caused it. Timing matters because insurers compare your claim against local weather records, and a clear connection between the damage and a known storm event makes approval much more likely.

Standard homeowners policies list specific perils they cover, and everything outside that list gets denied. Wind, hail, fire, and falling objects like tree limbs typically make the covered list, along with damage from the weight of ice or snow in rare Texas freezes. What doesn't make the list matters just as much, since insurers exclude damage tied to age, neglect, or poor maintenance almost every time.

Adjusters look for patterns that point to wear rather than a single event. Common exclusions include:

A roof that fails from years of wear won't get the same payout as one destroyed in a single storm.

Some policies also apply an actual cash value payout for older roofs instead of full replacement cost, which shrinks your settlement significantly. Reading your policy's peril list and depreciation schedule before disaster strikes tells you exactly where you stand.

Filing fast matters as much as filing correctly. Most Texas policies set a claim deadline ranging from a few months to a year after the storm, so don't sit on obvious damage hoping it resolves itself.

Work through these in order:

The homeowner who shows up with organized documentation almost always gets a fairer settlement than one who waits for the adjuster to find everything.

An adjuster works for the insurance company, not for you. A contractor-led assessment, especially one with detailed photo documentation, gives you a second set of eyes that can catch damage the adjuster's walkthrough misses, particularly on steep or hard-to-reach sections of the roof.

Getting a fair settlement rarely happens by accident. Insurance adjusters work fast, and they're trained to minimize payouts, so the burden falls on you to prove the full scope of damage before repairs begin. Homeowners who document thoroughly and negotiate confidently walk away with settlements that actually cover the real cost of a new roof.

Strong documentation changes the outcome of a claim more than almost anything else. Before you accept an adjuster's estimate, gather:

A claim backed by 100+ photos is far harder for an insurer to underpay than one built on a quick walkthrough.

Never treat the adjuster's first number as final. Roofing contractors who specialize in insurance claims can spot underestimated scope, missing flashing damage, or mismatched shingle counts that adjusters overlook. Requesting a re-inspection with that documentation in hand often raises the settlement enough to cover the full replacement, not just a patch job.

Knowing whether your policy covers roof damage isn't just paperwork, it's what stands between you and a repair bill you didn't budget for. The line between a covered storm claim and a denied one usually comes down to timing, documentation, and how clearly you can connect the damage to a specific event. Homeowners who understand their coverage before a storm hits, not after, make faster decisions and get fairer settlements.

If a recent storm has you wondering about the condition of your roof, don't guess. Defend Roofing offers a documented, 100+ photo Precision Roof Assessment that gives you clear evidence of what's damaged, what's covered, and what your insurer needs to see. Chris and Greyson bring three generations of roofing experience to every inspection, and they'll tell you honestly whether you need a repair or a full replacement.

Ready for straight answers? Reach out for your instant quote and get a professional on your roof before your claim window closes.