Does insurance cover roof replacement? Learn how age and policy types affect your payout, plus get tips to navigate the claims process and avoid denials.

Your roof takes a hit during a storm, and the first question is usually: does insurance cover roof replacement, or are you paying out of pocket? The answer depends on several factors, what caused the damage, how old your roof is, and what your specific policy actually says. Not every claim gets approved, and not every denial is final.

At Defend Roofing, we help Central Texas homeowners work through this process every week. As a family-owned roofing contractor with three generations of experience, we've seen how proper documentation and honest assessments make the difference between a covered claim and a denied one. Our 100+ photo Precision Roof Assessments give adjusters exactly what they need to evaluate your claim fairly.

This article breaks down when insurance typically pays for a roof replacement, how your roof's age affects your payout, and what the claims process looks like from start to finish, so you know where you stand before you file.

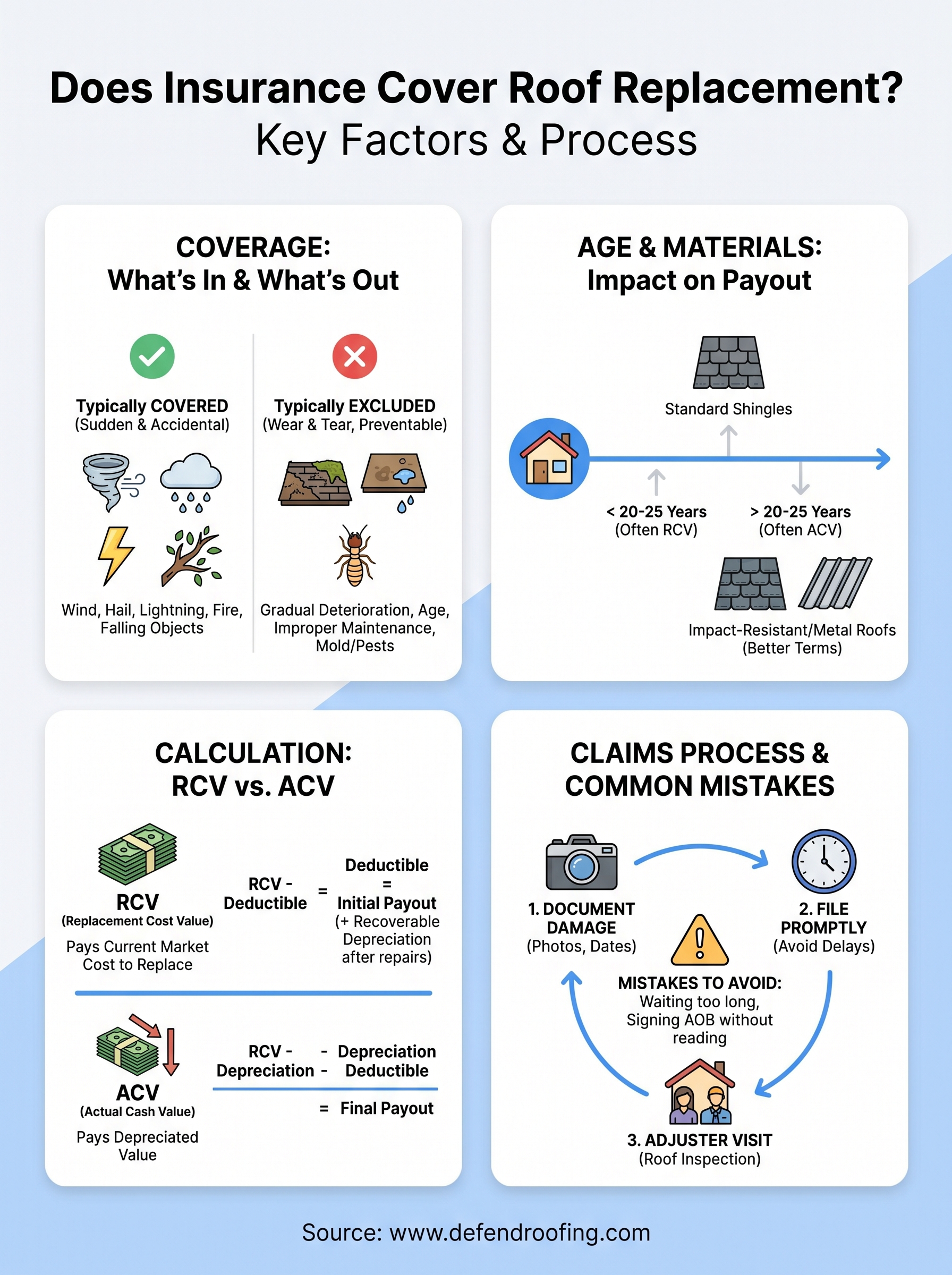

When you ask does insurance cover roof replacement, the honest answer is: it depends on the cause. Most standard homeowners policies cover sudden and accidental damage from specific events, called covered perils. They do not cover gradual deterioration or damage you could have prevented with routine maintenance.

Wind and hail damage are the two most common reasons homeowners file a roof claim in Central Texas, and both fall under most standard policies. Fire, lightning, falling objects, and certain types of water damage from sudden events also make the covered perils list. If a storm tears off shingles, cracks flashing, or dents your metal roof, that is the kind of event your insurer expects to pay for.

The key word here is "sudden." If damage traces back to a single storm event, you have a strong foundation for a covered claim.

Your policy documents will list the covered perils specifically. Reviewing your declarations page before a storm hits is worth the 10 minutes it takes, because surprises during a claim cost you time and money.

Insurance companies do not pay for wear and tear, and this is where most denials happen. If your roof is deteriorating because of age, missing granules from normal weathering, or long-standing leaks you never addressed, the insurer will classify that as a maintenance issue and reject the claim.

Improper installation and manufacturer defects also fall outside standard coverage. If the original roofer cut corners, that liability goes back to the contractor, not your insurer. Mold and pest damage follow the same logic: insurers treat them as preventable, not sudden. Knowing these exclusions upfront keeps your expectations realistic before you file.

Your roof's age and material type shape your coverage options more than most homeowners expect. Insurers factor both into how much they'll pay and under what terms before they approve a claim.

Most insurers draw a line around 20 to 25 years for standard asphalt shingle roofs. If yours falls under that threshold, you likely qualify for replacement cost value (RCV) coverage, meaning the insurer pays to replace it at current market prices.

Once a roof passes that age window, many policies shift to actual cash value (ACV), which subtracts depreciation and cuts your payout significantly.

ACV policies leave you covering the gap between what the insurer pays and what replacement actually costs, which can run into thousands of out-of-pocket dollars on an older roof.

Metal roofs and impact-resistant shingles often earn better coverage terms. Many insurers extend RCV eligibility longer for these materials because they handle hail and wind better than standard asphalt options.

When you ask does insurance cover roof replacement, your material choice directly influences the answer. Upgrading to a Class 4 impact-resistant shingle at replacement time can lower your premium and lock in stronger coverage going forward.

Understanding your payout starts with knowing which coverage type your policy uses. When you ask does insurance cover roof replacement, the dollar amount you receive depends on the calculation method your insurer applies, not just whether the claim gets approved.

Replacement cost value (RCV) pays what it actually costs to replace your roof today, using current labor and material prices. Your insurer typically releases this in two stages: an initial payment minus depreciation, then a second payment called the "recoverable depreciation" once the work is complete and you submit the contractor invoice.

With ACV policies, that withheld depreciation never comes back to you, which is why knowing your policy type before you file matters.

Actual cash value (ACV) subtracts depreciation from that replacement cost before cutting your check. An older roof depreciates significantly, so your payout shrinks in proportion to the age of the roof.

Your deductible comes off the top of whatever the insurer calculates, whether RCV or ACV. If your insurer calculates a $12,000 replacement and your deductible is $2,000, your check is $10,000 before recoverable depreciation factors in.

Knowing the steps before you file keeps the process moving and reduces the chance of a denial. Filing promptly and with thorough documentation shapes the outcome as much as your policy does. When you ask does insurance cover roof replacement, the process itself can determine whether you get paid.

A poorly documented claim or a missed reporting deadline can cost you coverage even when the damage clearly qualifies.

Photograph everything before anyone touches the roof. Capture damage from multiple angles, including close-ups of cracked or missing shingles, dented flashing, and granule loss in gutters. Your documentation becomes the foundation of the adjuster's evaluation, and gaps in evidence give insurers room to dispute the scope or cause.

Contact your insurer as soon as possible after the storm. Most policies require prompt reporting, and delays give insurers grounds to question whether conditions worsened while you waited.

Once you file, the insurer schedules an adjuster inspection. Having a roofer present during that visit helps you identify damage the adjuster might overlook and address technical questions in real time.

Homeowners asking does insurance cover roof replacement often run into the same avoidable mistakes. Understanding where claims go wrong helps you protect your payout and your timeline before and after you file. Two issues come up more than any others: delayed filing and misunderstood paperwork.

Delay is one of the fastest ways to lose a valid claim. Most policies require you to report damage within a reasonable timeframe, and some set specific deadlines as short as one year. When you wait weeks or months after a storm, the insurer gains room to argue that conditions worsened because of inaction, not the original event itself.

Filing within days of a storm gives you the strongest position and leaves no room for dispute over timing.

Assignment of benefits (AOB) agreements let contractors collect your claim payment directly from the insurer. While that sounds convenient, signing over your claim rights before you fully understand the scope locks you into terms you may not control. Read every document carefully before you sign, and make sure your contractor gives you a clear breakdown of the work and the cost before anyone touches your roof.

If you've been asking does insurance cover roof replacement after recent storm damage, the next move is getting a thorough, documented assessment before you file. What your adjuster sees during inspection determines your payout more than almost anything else, and walking into that process with clear photo evidence puts you in the strongest possible position. Coverage depends on the cause of damage, your roof's age, and your policy type, but none of that matters if your documentation leaves gaps that the insurer can dispute.

Defend Roofing's Precision Roof Assessment gives you 100+ photos and a written damage evaluation that your insurer can act on directly. We serve Central Texas homeowners in Austin, Cedar Park, Leander, and the surrounding area, and we coordinate with your adjuster to make sure the full scope of damage gets on record. Schedule your roof assessment today and walk into the claims process with the documentation your insurer needs to pay the claim.