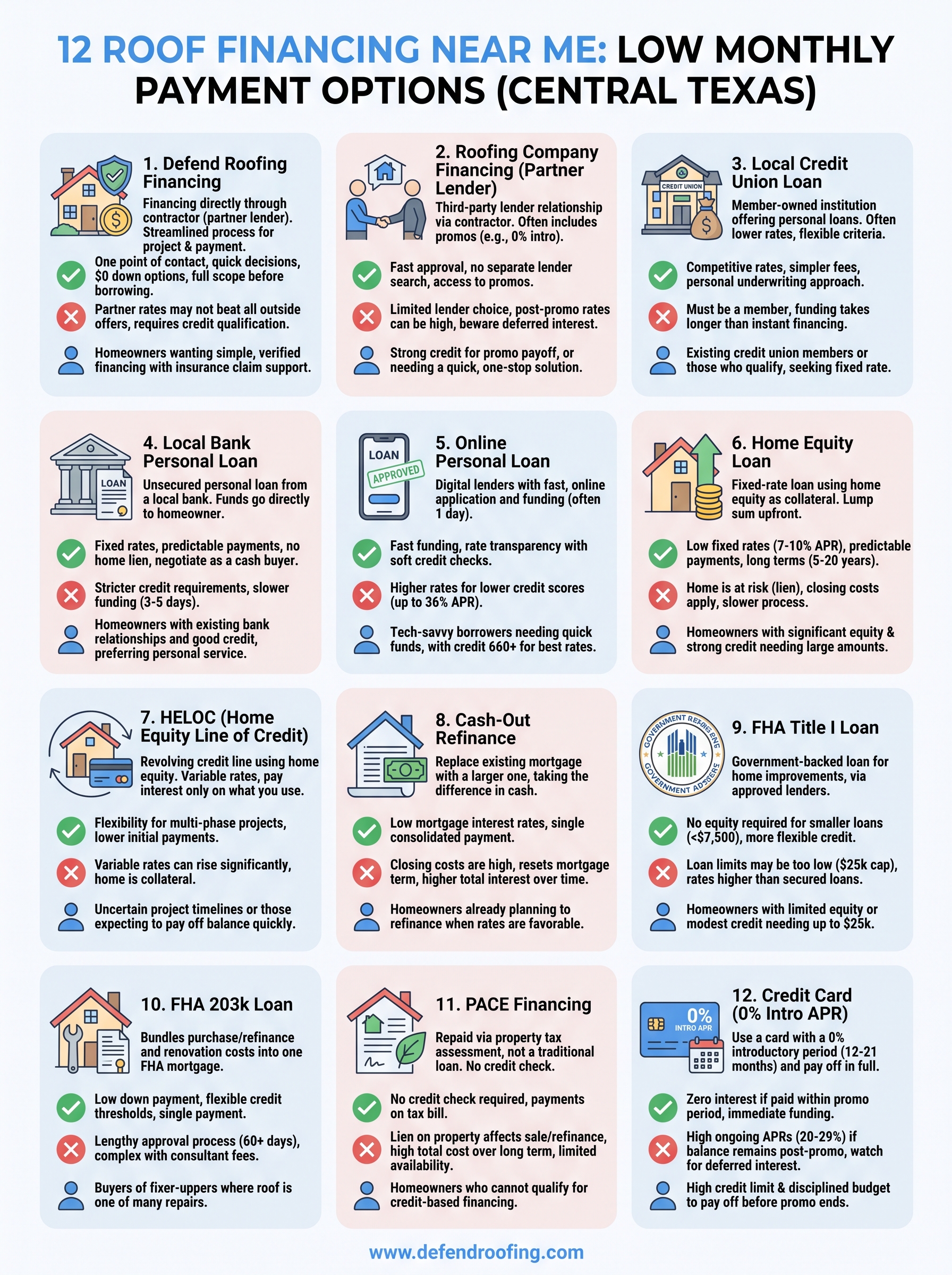

Find 12 roof financing near me options for low monthly payments. Compare zero-down plans, home equity, and FHA programs to fund your roof replacement.

A full roof replacement in Central Texas typically runs between $8,000 and $15,000 or more, depending on size, materials, and complexity. That's not a number most homeowners can pull from savings without feeling the hit. If you've been searching for roof financing near me, you're probably trying to figure out how to get the work done without draining your bank account or settling for a subpar contractor just because they're cheap.

The good news: you have more financing options than you might think. From roofing company in-house plans to personal loans, home equity products, and government programs, there are real paths to manageable monthly payments, even if your credit isn't perfect. The key is understanding what each option actually costs you over time, not just what the monthly number looks like.

At Defend Roofing, we're a family-owned contractor serving Austin and the surrounding Central Texas communities, and we help homeowners navigate this exact decision regularly. We offer financing options for qualified homeowners and walk you through the full picture, what you'll pay, what the terms mean, and whether financing or an insurance claim makes more sense for your situation. No pressure, no hidden nonsense.

This article breaks down 12 roof financing options available to Central Texas homeowners, covering how each one works, what to watch out for, and which situations they fit best. By the end, you'll know exactly which route makes sense for your budget and your roof.

Defend Roofing is a family-owned roofing contractor serving Austin and Central Texas, operated by Chris and Greyson Buster with three generations of roofing experience between them. Beyond replacing and repairing roofs, the company offers financing options for qualified homeowners so that cost doesn't force you into a bad decision, like skipping necessary work or hiring a cheap contractor you can't trust.

Roof replacements and major repairs are both eligible under Defend Roofing's financing program. If you've been searching for roof financing near me and want to keep things simple, financing through your contractor means one conversation covers both the project and the payment plan. You won't need to coordinate a separate lender while also managing materials, timelines, and inspections.

Defend Roofing starts every project with a Precision Roof Assessment that includes 100+ photos documenting exactly what your roof needs. After you receive a clear, honest recommendation, you apply through the partner lender. Approval decisions typically come back quickly, so you know your borrowing amount before any work begins.

Knowing your exact project scope before applying means you borrow what you actually need, not a rough estimate that could leave you short or overextended.

Rates and terms depend on your credit profile and loan amount. Qualified borrowers may access $0 down options, with repayment structured to keep monthly costs predictable. Ask the Defend Roofing team about current lender promotions, since these programs update periodically.

The partner lender sets the qualification criteria, but typical requirements include:

Defend Roofing can explain what the lender generally looks for so you go in with realistic expectations.

Pros include a single point of contact, full project documentation before you borrow, $0 down options for qualified buyers, and a Limited Lifetime Workmanship Warranty backing the installation.

Cons include the fact that partner lender rates may not beat every outside offer, and borrowers with low credit scores may not qualify, requiring a different financing path.

This option fits Central Texas homeowners who want to finance a replacement or significant repair through a contractor they can verify and trust. It's especially practical for homeowners who also need insurance claim support, since Defend Roofing handles adjuster coordination alongside the project itself.

Before you commit, get clear answers on:

Contact Defend Roofing to schedule your free Precision Roof Assessment. Once you have a documented project cost, you can apply for financing with a real number in hand rather than a guess. The team walks you through each step from inspection to installation.

Many roofing contractors offer financing through a third-party lender they've established a relationship with. This is one of the most common setups homeowners find when searching for roof financing near me, and it often means you can apply during the same appointment where you get your estimate.

The contractor connects you with a specialty home improvement lender. You fill out a short application, often on a tablet during the sales visit, and receive a decision within minutes. If approved, the lender pays the contractor directly, and you make monthly payments to the lender, not the roofing company.

Contractors frequently advertise lender promotions to close deals. Common offers include:

Outside any promotional period, rates typically run from 9% to 29% APR, depending on your credit profile. Loan amounts generally cover $2,500 to $55,000, which handles most residential roofing projects.

Pros include fast approvals, no need to find your own lender, and access to promotional rates that can work in your favor. Cons include limited lender choice since the contractor picks the partner, and post-promo rates can be significantly higher than what you'd find elsewhere.

Homeowners with strong credit scores who can confidently pay off the balance before a promo period ends, or those who want a straightforward, one-appointment process without coordinating separate financing.

Watch closely for deferred interest clauses, where the full interest accrues from day one and gets added to your balance if you miss the payoff deadline. Also check for origination fees and prepayment penalties before you sign anything.

Read the complete loan agreement yourself, not just the monthly payment summary handed to you during the sales visit.

Before committing, get a quote from a credit union or online lender to compare APRs. If the partner lender's rate after the promo period is higher, a fixed-rate outside loan will almost always cost you less over the full repayment term.

Credit unions are member-owned financial institutions that typically offer lower rates and more flexible lending criteria than commercial banks. If you've been searching for roof financing near me and your roof work doesn't involve major structural changes, a local credit union home improvement loan is worth a serious look.

You apply directly with a credit union for an unsecured or secured personal loan earmarked for home improvement. Once approved, funds land in your account, and you pay your roofing contractor directly like a cash customer. This gives you negotiating power on price since the contractor isn't waiting on a third-party lender.

Credit unions frequently offer rates between 7% and 18% APR, which is often meaningfully lower than contractor partner lenders. Loan terms typically run 24 to 84 months, and loan amounts commonly reach $25,000 to $50,000 for home improvement purposes.

Pros include competitive rates, nonprofit status that keeps fee structures simpler, and loan officers who often take a more personal approach to borderline applications. Cons include the fact that you must be a member to borrow, and approval timelines can run several business days longer than instant contractor financing.

Homeowners who are already credit union members or who qualify for membership through their employer, location, or family. It also suits borrowers who want a straightforward fixed-rate loan without lender-specific promotional conditions.

Most credit unions require a minimum credit score around 620 to 660, steady income documentation, and an acceptable debt-to-income ratio. Membership must be established before you can apply for a loan.

Joining a credit union before you need the money saves time when a roof problem becomes urgent.

Search the National Credit Union Administration's credit union locator at mycreditunion.gov to find federally insured options in your area.

Ask about the full APR, any origination fees, prepayment penalties, and how long funding takes after approval so you can plan your project start date accurately.

Local banks offer personal loans that can cover a full roof replacement without requiring you to put up your home as collateral. If you already have a checking or savings account at a community bank, you may find the application process more personal than going through an online lender when searching for roof financing near me.

You apply at the bank for an unsecured personal loan, receive a lump sum after approval, and pay your roofing contractor directly. Because funds go straight to you, you can negotiate pricing with contractors the same way a cash buyer would, which sometimes yields a better deal than financing arranged through the contractor.

Bank personal loan rates generally fall between 8% and 24% APR, with existing customers sometimes receiving preferred rates. Repayment terms typically run 12 to 60 months, and loan amounts at community banks commonly reach $15,000 to $35,000, which covers most standard residential roofing projects.

Pros include fixed interest rates, predictable monthly payments, and no lien placed on your home. Cons include stricter credit requirements than many credit unions and slower funding timelines than online lenders, sometimes taking three to five business days after approval.

An existing banking relationship can work in your favor during underwriting, especially if your credit profile has a few rough spots.

Homeowners who already bank locally and prefer working with a person rather than an app. It also suits borrowers who want a fixed-rate, no-collateral loan and who have a few days to wait for funding before scheduling their roofing project.

Banks typically require a credit score of 660 or higher, verifiable income, and a debt-to-income ratio below 40%. Existing account holders with a positive payment history often have a stronger shot at approval and may receive slightly lower rates than new applicants.

Visit two or three local branches and ask each one for a written loan estimate that includes the full APR, total repayment cost, fees, and prepayment terms before committing to anything.

Online lenders have made it faster than ever to secure roof financing near me without setting foot in a bank branch. You apply entirely through a website or app, receive a decision within minutes to a few hours, and get funds deposited directly to your bank account, often as quickly as one business day after approval.

You submit an application on the lender's website with basic personal, income, and employment information. The lender runs a hard credit pull to finalize your offer, and if approved, sends the loan amount directly to your bank account. You then pay your roofing contractor like a cash customer, which keeps you in full control of vendor selection and project negotiation.

Online personal loan rates generally range from 7% to 36% APR, depending heavily on your credit profile. Loan amounts typically fall between $1,000 and $50,000, with repayment terms of 24 to 84 months. Borrowers with strong credit scores frequently land rates competitive with or better than what local banks offer.

Fast funding and rate transparency are the biggest advantages. Most reputable online lenders show you personalized rate estimates through a soft credit check before you formally apply, so there are no surprises at signing. The main downside is that borrowers with lower credit scores can face rates well above 25% APR, making other options more cost-effective.

Online personal loans work well for homeowners who want quick funding without tapping home equity or waiting on a bank's slower underwriting process. They suit borrowers who are comfortable applying digitally and who have a credit score of 660 or higher to access competitive rates.

Your credit score, debt-to-income ratio, loan amount, and repayment term all influence the rate you receive. A longer repayment term lowers your monthly payment but raises the total interest you pay over the life of the loan.

Always check whether the lender charges an origination fee, since a fee of 1% to 6% of the loan amount can significantly change the true cost of borrowing.

Use pre-qualification tools on multiple lender websites to collect rate estimates with soft credit pulls before committing. Compare the full APR, origination fees, total repayment cost, and funding timeline side by side rather than focusing only on the monthly payment figure.

A home equity loan lets you borrow a lump sum against the equity you've built in your property. If you've been searching for roof financing near me and you own your home with significant equity, this option often delivers some of the lowest interest rates available for a major roofing project.

You borrow a fixed amount based on your home's appraised value minus your remaining mortgage balance. The lender gives you the full sum upfront, you pay your contractor, and you repay the loan in fixed monthly installments over the agreed term.

Home equity loan rates generally run between 7% and 10% APR for borrowers with strong credit, significantly lower than most unsecured personal loans. Terms range from 5 to 20 years, and closing costs typically add 2% to 5% of the loan amount, so factor that into your total project cost.

Fixed rates and predictable payments make budgeting straightforward for the entire repayment period. The downside is that your home secures the debt, meaning a missed payment puts your property at risk, and closing costs make small loan amounts harder to justify economically.

Homeowners with substantial equity and strong credit who need to borrow more than $20,000 and want a low, fixed rate over a longer repayment term.

Most lenders require a credit score of 680 or higher, a combined loan-to-value ratio below 85%, and verifiable income that supports the added monthly payment alongside your existing mortgage.

Expect the process to take three to six weeks from application to funding, since the lender requires a property appraisal before approving your loan amount.

If your roof is actively leaking, a home equity loan's timeline may be too slow to protect your home from further damage.

Because your home serves as collateral, defaulting on this loan carries consequences far beyond a credit score hit. Only borrow what the project genuinely requires.

A Home Equity Line of Credit (HELOC) gives you access to a revolving credit line based on your home equity, rather than a single lump sum. If you're searching for roof financing near me and your project scope might shift during construction, a HELOC offers flexibility that a standard home equity loan does not.

A HELOC operates much like a credit card secured by your home. During the draw period, typically 5 to 10 years, you pull funds as needed up to your approved credit limit and make interest-only payments on what you've borrowed. After the draw period closes, repayment begins on the full outstanding balance.

HELOCs carry variable interest rates that typically start between 8% and 11% APR for qualified borrowers. Most lenders set a minimum draw amount and require that you maintain a loan-to-value ratio below 85% throughout the draw period.

Flexibility and lower initial payments are the main advantages. You only pay interest on what you actually use, which helps if your roofing project runs over budget or expands in scope. The drawback is that variable rates can rise significantly over a multi-year repayment window, making total costs harder to predict.

Homeowners managing a multi-phase project or those who want access to funds without committing to a fixed loan amount upfront benefit most from a HELOC.

Lenders generally require a credit score of 680 or higher, a combined loan-to-value ratio below 85%, and steady, verifiable income sufficient to cover both your existing mortgage and new credit line payments.

Your rate ties directly to a benchmark index, often the prime rate. When that index rises, your payment rises with it, sometimes substantially. Budget for a rate increase of 2 to 3 percentage points above your starting rate when calculating affordability.

If interest rates are already elevated or trending upward, locking into a fixed-rate home equity loan typically saves you money over the full repayment term.

A HELOC makes more sense than a home equity loan when your project timeline is uncertain or when you expect to pay off the balance quickly during the lower-rate draw period, minimizing total interest paid.

A cash-out refinance replaces your existing mortgage with a new, larger loan and puts the difference in your pocket. If you've built up equity and current mortgage rates work in your favor, this can be a practical way to fund a roof replacement while keeping everything under one monthly payment.

You apply for a new mortgage that pays off your current loan balance, with the extra amount above that balance issued to you as cash at closing. You then pay your roofing contractor directly and repay the new loan through your regular monthly mortgage payment at the new rate and term.

A cash-out refinance works best when current mortgage rates are lower than your existing rate, meaning you're not paying more to refinance than you would through separate financing. If rates have risen since you originated your mortgage, this option typically costs more over time than a standalone personal loan or home equity product.

Expect closing costs of 2% to 5% of the new loan amount, and budget four to seven weeks from application to funding since lenders require a full appraisal and underwriting review before approving the transaction.

Low interest rates and a single consolidated payment make this option attractive when the math works out. The downside is that you reset your mortgage term, potentially adding years of payments and significantly increasing the total interest paid over the life of the loan.

Homeowners who already planned to refinance for rate or term reasons and want to roll roof costs into that transaction rather than taking on a separate debt product at the same time.

If a cash-out refinance is your only reason to refinance, run the full numbers first, because closing costs alone can easily exceed $5,000 on a typical home loan.

Compare the total loan cost over the full repayment term, not just the monthly payment or the stated rate, against what a home equity loan or personal loan would cost you for the same roof project.

Your home secures the entire debt, and resetting a 30-year mortgage to access $10,000 for roof financing near me needs can cost far more in long-term interest than any short-term savings on your monthly rate.

The FHA Title I program is a government-backed loan designed specifically to help homeowners fund improvements that protect and maintain their property. If your equity is limited or your credit history is thinner than you'd like, this program can open doors that conventional lenders might close when you're searching for roof financing near me.

Title I is managed by the U.S. Department of Housing and Urban Development (HUD) and allows approved private lenders to offer home improvement loans with federal backing. That backing reduces the lender's risk, which means lenders can approve borrowers who might not qualify for a standard personal loan or home equity product on their own.

You apply through an FHA-approved lender, not through the government directly. Once approved, funds go to you or directly to your contractor, and the loan covers eligible improvements including roof replacement and repair. HUD classifies roofing work as a qualifying home improvement, so the project type fits the program well.

For single-family homes, unsecured Title I loans cap at $25,000, which covers most standard residential roofing projects. Key details include:

No equity required for loans under $7,500, and credit requirements tend to be more flexible than conventional loans. The downside is that loan limits may fall short for large or complex projects, and rates can run higher than a home equity loan since smaller amounts aren't fully secured by the property.

If your roof replacement estimate falls under $25,000, Title I is worth comparing directly against personal loan offers before you commit to either.

Homeowners with limited equity or modest credit profiles who need up to $25,000 for a roof replacement and want a government-backed option with longer repayment terms than most unsecured personal loans provide.

Visit HUD's official lender search at hud.gov to locate approved lenders in your area. Contact at least two lenders to compare rates and fees side by side before submitting a formal application.

The FHA 203k loan is a government-backed mortgage program that combines the cost of purchasing or refinancing a home with the cost of renovations into a single loan. If your roof replacement is part of a broader set of repairs, this program lets you bundle everything into one monthly payment rather than managing multiple debts simultaneously.

The FHA 203k is administered through HUD-approved lenders and insured by the Federal Housing Administration. Unlike the Title I loan, which functions as a standalone improvement loan, the 203k ties directly to your mortgage balance, making it a fundamentally different product suited to different situations.

You work with an approved lender and an HUD consultant who documents the required repairs and verifies that your roofing project meets program guidelines. The lender rolls the renovation costs into a new FHA mortgage, and funds are disbursed to your contractor in draws as work progresses rather than as a lump sum upfront.

This draw structure means your contractor needs to be comfortable waiting on staged payments, so confirm this arrangement before committing to the 203k process.

The 203k makes the most sense when you are buying a home that needs significant roof work before you move in, or when you are refinancing and need to address multiple repairs at once. If a roof replacement is your only project, simpler financing options like a personal loan or FHA Title I will get you funded faster with far less paperwork.

Low down payment requirements and flexible credit thresholds make this program accessible to buyers who cannot qualify for conventional renovation financing. The downside is a lengthy approval and disbursement process that can stretch to 60 days or more, plus the added cost of required consultant fees and a more complex closing process.

Homebuyers purchasing a fixer-upper property where roof replacement near me is one of several necessary repairs that sellers won't address before closing.

You need a minimum credit score of 580 for the standard 3.5% down payment option. Plan for a 45 to 60-day timeline from application to closing, and budget for consultant fees that typically run between $400 and $1,000 depending on project complexity.

PACE (Property Assessed Clean Energy) financing lets you fund home improvements through an assessment attached to your property tax bill rather than a traditional loan. It's an unconventional option when searching for roof financing near me, and it comes with significant trade-offs worth understanding before you apply.

A PACE lender pays your roofing contractor directly, and you repay the amount through an additional line item on your property tax bill each year. Because repayment runs through the tax system rather than a personal lender, approval typically doesn't depend on your credit score.

PACE programs are not available in every state, and availability varies at the county level even where state law permits them. Texas currently has limited PACE availability primarily focused on commercial properties, so Central Texas homeowners should confirm residential eligibility before pursuing this route.

Repayment terms typically run 5 to 25 years, with annual assessments added to your property tax payment. Interest rates generally fall between 5% and 9%, though the total cost over a long term can exceed what a shorter personal loan would cost you.

No credit check and direct contractor payment are clear advantages for borrowers who cannot access traditional financing. The downside is that the lien attached to your property sits ahead of your mortgage lender's claim, which creates complications if you sell or refinance.

Before signing any PACE agreement, confirm in writing how the assessment affects your ability to refinance your mortgage.

Homeowners in states with active residential PACE programs who cannot qualify for any credit-based financing and need an alternative path to fund a necessary replacement.

PACE assessments transfer with the property at sale, meaning a buyer must either assume your remaining balance or you pay it off at closing. Many buyers and their lenders will reject properties carrying an active PACE lien.

Ask the PACE provider for the full total repayment cost, how the lien is disclosed at sale, and whether your current mortgage servicer permits a senior PACE assessment on the property.

A credit card with a 0% introductory APR is one of the most overlooked options when homeowners search for roof financing near me. If your project cost falls within your available credit limit and you can pay off the balance before the promo period ends, this approach can be the cheapest financing method available, period.

You open or use an existing credit card offering a 0% APR promotional period, typically ranging from 12 to 21 months, and charge your roofing project to that card. During the promo window, no interest accrues on your balance as long as you make minimum payments on time. Pay the full balance before the period ends, and you've essentially borrowed money at zero cost.

This option beats every other financing method when your project cost is manageable enough to eliminate within the promotional window. For example, a $6,000 repair paid over 18 months requires roughly $333 per month. If you can maintain that pace, you pay nothing beyond the project price itself.

This only works if you treat the payoff deadline as a hard commitment, not a loose goal.

Zero interest during the promo period and immediate access to funds are the clear advantages. The downside is that credit cards carry high ongoing APRs, often 20% to 29%, which kick in the moment your promotional window closes on any remaining balance.

Homeowners with a high enough credit limit to cover the project and a realistic monthly budget to pay it off before the promo period expires.

Mark the exact expiration date on your calendar and confirm whether the card uses deferred interest or true 0% interest. These two structures look identical upfront but behave very differently if you carry a balance past the deadline.

Divide your total balance by the number of promo months and set that as your automatic monthly payment. This keeps you on track to clear the debt before the standard rate applies.

You now have a clear picture of the 12 roof financing near me options available to Central Texas homeowners, and each one works differently depending on your situation. The right choice depends on your credit profile, equity position, and how quickly you need the work done. Start by pinning down an accurate project cost so you're borrowing a real number rather than a rough estimate that could leave you short or overextended.

From there, compare two or three options using full APR and total repayment cost, not just the monthly payment. That single comparison will reveal which path actually costs you less over the full term.

If you're in the Austin area or surrounding Central Texas communities, Defend Roofing will assess your roof with 100+ photos and a transparent repair-vs-replace recommendation before you spend anything. You can then apply for financing with a concrete number in hand and move forward with confidence. Schedule your free Precision Roof Assessment and get a quote today.